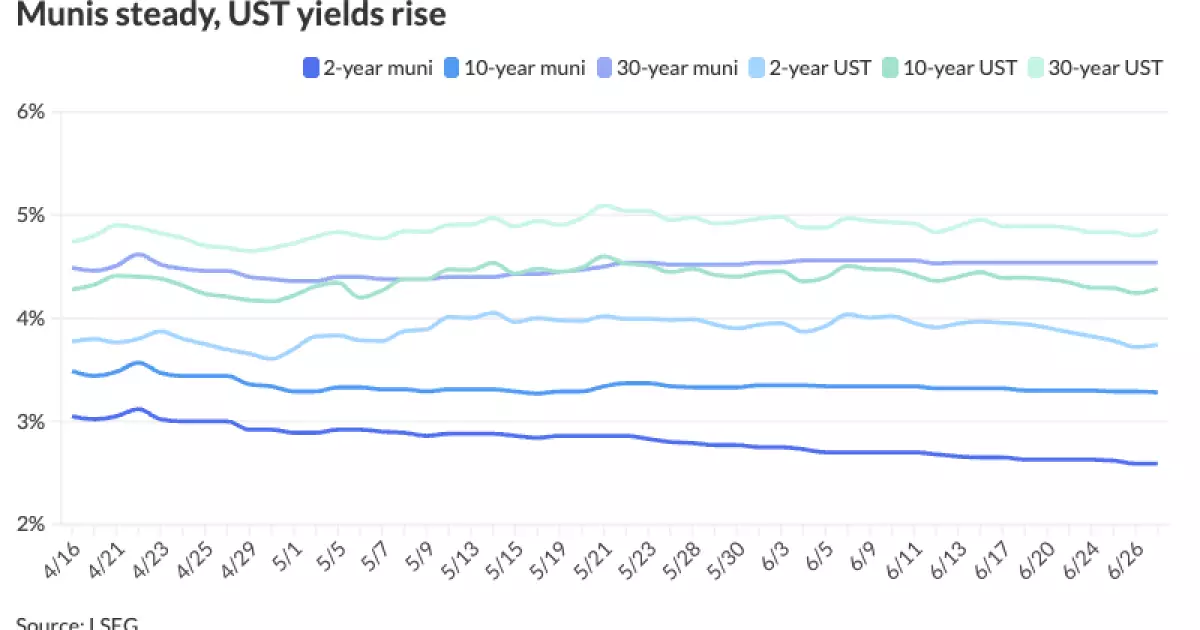

At first glance, the municipal bond market might appear stable with steady prices and record highs in equities. However, beneath this surface lies a more troubling and complex reality that investors and policymakers must confront. Municipal bonds, despite their reputation as safe havens for conservative investors, have underperformed significantly in the first half of 2025. They remain the only fixed income category posting negative total returns year-to-date, a fact that signals a waning confidence in what has traditionally been a dependable asset class.

This fragility stems not only from evolving macroeconomic pressures but also from an unprecedented surge in supply that threatens to overwhelm the market’s absorption capacity. While U.S. Treasury yields climb and stocks rally, municipals have struggled to keep pace, revealing intrinsic weaknesses that are often masked by superficial market optimism.

Supply Shock: The Elephant in the Room

The deluge of new municipal bond issuance this year is staggering. For June alone, issuance is poised to top $50 billion, marking the largest monthly issuance forecast for 2025 so far. Projections for the entire year have been revised upwards, with some institutions like BofA Securities now estimating supply will hit $580 billion—far exceeding earlier estimates of $520 billion. This explosion in supply puts significant downward pressure on municipal bond prices and directly contributes to their disappointing performance.

It’s essential to see this flood of issuance as more than just a technical market event—it signals underlying fiscal stress at the state and local government level. Many municipalities are turning to debt issuance aggressively, attempting to finance infrastructure, public services, and pension liabilities amid tightening budgets and rising interest rates. This borrowing binge is unsustainable; it raises long-term concerns about credit quality and market stability that few are addressing explicitly.

Demand Dynamics and Ratios That Worry

As issuance skyrockets, demand and relative value have shifted unfavorably for municipals. The muni-to-Treasury ratio—a key metric indicating relative value between tax-exempt municipal bonds and risk-free Treasuries—has risen notably, especially for longer maturities. Ratios for 10-year and 30-year maturities have surged by several percentage points, reflecting municipals’ underperformance against Treasuries.

While some strategists optimistically argue that ratios typically decline in July and August, suggesting a seasonal rebound driven by technical factors like redemptions and coupon payments, this perspective feels overly sanguine. A seasonal dip in issuance cannot mask the structural oversupply problem. Moreover, the typical seasonality assumes stable or improving fiscal health among municipalities, a premise increasingly undermined by economic stagnation in many local economies.

The Mirage of “Value” in Today’s Fixed Income Market

Market experts who tout current muni valuations as “good value” deserve scrutiny. While it’s true that depressed prices create buying opportunities, these valuations cannot be divorced from broader economic and fiscal realities. Labeling municipals as fundamentally cheap ignores the question: cheap for what risk profile?

Investors need to be cautious about interpreting present yields and spreads as signals to load up on long-duration municipals. In a rising rate environment with downbeat growth prospects and fiscal strain, yields baking in modest risks may swiftly become insufficient compensation. The presumption that rates will stabilize or that performance will “back-load” later in the year is an optimistic forecast that discounts both potential economic headwinds and political impediments to remedying municipal balance sheets.

Political Risks Lurk Amid Fiscal Reckoning

From a center-right perspective, one glaring omission in conventional municipal market analysis is the critical lens on government fiscal discipline and structural reform. Excessive borrowing by municipalities is not merely a market cycle but a symptom of ongoing governance failures: inefficient spending, reluctance to make hard choices on pensions and public services, and unwillingness to reform tax policies to create sustainable revenue streams.

If Washington continues to encourage more spending without demanding reform, municipal credit deterioration will accelerate. Investors should not be lulled into complacency by record equity markets or short-term tactical plays. True resilience in municipal bonds will only emerge through disciplined fiscal management, streamlined government services, and genuine structural reforms that reduce dependency on borrowing.

Looking Ahead: A Call for Prudence and Reform

Investors eyeing the municipal bond market should approach with a healthy skepticism and recognition of the fragility beneath headline stability. The market may appear “steady” for now, but the perfect storm of record issuance, rising yields, and persistent fiscal imbalances forewarns of turbulence ahead.

Long-term confidence in munis depends not on cyclical technicals but on fundamental shifts in governance and spending priorities. Until state and local governments embrace fiscal responsibility, the municipal bond market will remain vulnerable to shocks that could reverberate far beyond a mere adjustment in ratios or issuance calendars. Those who overlook these realities do so at their peril.

Leave a Reply