In an unexpected turn, President Trump’s decision to impose a 90-day hiatus on his typical retaliatory tariff strategy sent shockwaves through the municipal bond market. The initial fallout was mixed; we witnessed AAA yields plunge by 30 to 50 basis points on Thursday, only to recover some footing following a tumultuous week of trading. What this volatility essentially showcases is not merely erratic trading patterns but a market grappling with uncertainty and shifting sentiments about economic stability.

The municipal bond market thrives on predictability, and that has been sorely lacking. It’s reminiscent of a tug-of-war: while the bond yields made a significant rebound, the underlying fear is palpable. Investors are clearly still jittery after having experienced the worst single-day returns in over three decades earlier in the week, reflecting a historical pattern of volatility that affects even the most stable of asset classes.

Historic Slump: Analyzing the Recent Market Waves

The municipal bond sector is no stranger to tumultuous changes, but the recent drastic shifts in yields can hardly be ignored. Astoundingly, the combined yield adjustments of 90 basis points over just three days marked the second-largest movement observed since records began, following only the tumultuous period of the 1980s. This is a serious indictment of current market conditions and raises questions about the fundamentals that are driving these extraordinary shifts.

You’d think that such historical averages should provide a semblance of stability; however, they paint a rather unsettling picture. When liquidity plummets as experienced earlier this week, the consequences can escalate quickly. Leading investment figures like Sean Carney at BlackRock have pointed to the inherent lack of liquidity, indicating a fragile market percieved as being on the edge of a precipice. This raises crucial questions about resilience: can the municipal market recover, or are we merely witnessing band-aid solutions that gloss over deeper issues?

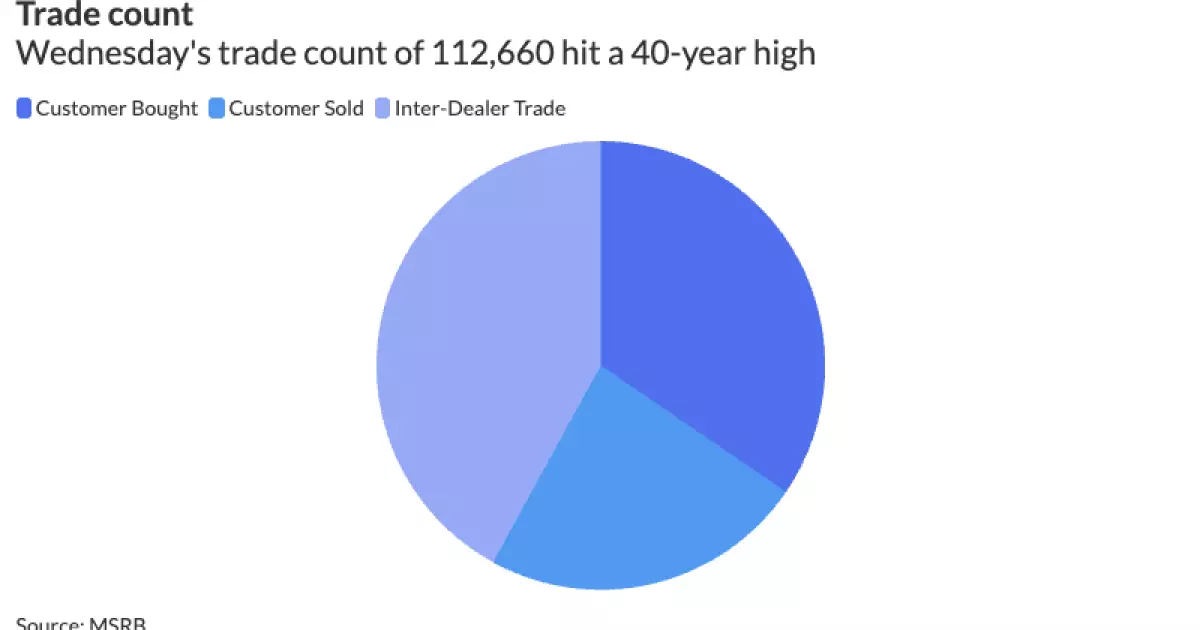

A Surge in Trade Activity Amidst Uncertainty

Despite the chilling effects on prices, one striking observation from recent weeks is the surge in trading activity. With an unprecedented 112,600 trades recorded on Wednesday alone, one could be forgiven for thinking the market was teeming with optimism. However, this uptick raises a paradox: increased trading volume does not necessarily equate to value or stability. It often indicates panic selling or significant positional adjustments rather than robust confidence in the market’s future.

The data show us that $32.5 billion changed hands, the highest amount since the early pandemic period. But this should serve as an alarm rather than a euphoric rallying cry. In the backdrop, it’s essential to corroborate these figures against the yield movements that preceded them. If the market is essentially reacting to fear as opposed to informed decision-making, we might be headed for an even more volatile phase.

Liquidity Crisis: What Lies Beneath the Surface

As discussions ensue about the spiral of yields and trading volumes, the underlying reality remains concerning. The liquidity crisis that many investors faced earlier this week signals a fundamental issue that cannot simply be brushed aside. When market liquidity dries up and investments turn into intangible assets almost overnight, it creates a paradox where sellers are left holding the bag with no viable exit strategies.

A market devoid of liquidity equates to a lack of trust, and this sentiment reverberates through all levels of investment, especially when discussing the future of municipal securities. If institutional investors begin to shy away due to these questions surrounding liquidity, the repercussions could be dire. In essence, while a momentary rebound is encouraging, what remains beneath the surface is a market that could lose its footing at the slightest hint of negative news.

Future Outlook: Cautiously Optimistic or Realistically Pessimistic?

In light of these unfolding events, one must wonder if the present dynamics of the municipal bond market can truly recover before larger systemic issues are resolved. The recent tariff announcement may have provided momentary relief, but the fundamental problems surrounding market liquidity and trust remain unaddressed. My speculation suggests that the next several weeks will testify to the strength or weakness of investor sentiment in this tumultuous arena.

Yet, one cannot ignore certain silver linings as June approaches—an anticipated uptick in redemptions and coupon payments could potentially inject some much-needed vitality back into the municipal market. However, the risk exists that such injections may only be temporary, potentially masking deeper issues that will demand attention down the line.

As time progresses, the municipal bond market stands at the precipice of profound change. Are we witnessing a remarkable rebound, or are investors simply waiting for the next shoe to drop? The volatility of the past week hints at an underlying concern: that the road ahead may be fraught with challenges more perilous than the ones we have just traversed.

Leave a Reply