In the current landscape of municipal bonding, the market exhibits notable trends as investors seek shelter and yield amidst a volatile economic environment. The juxtaposition of municipal bonds with U.S. Treasury yields reveals significant insights into market behavior, highlighting both performance metrics and investment strategies that are shaping this sector.

Recent market data indicates that municipal bonds, particularly those rated triple-A, have shown remarkable resilience despite a backdrop of weakening U.S. Treasury yields. As highlighted, while Treasury yields experienced a decline of three to four basis points, municipal bond yields remained virtually stagnant. This situation underscores the strength of the municipal sector, with investors seeing value even as Treasury securities falter. The unchanged yield curves of municipal bonds suggest a robust demand, reflecting the increasing preference for safer, more stable investments.

The recorded ratios between municipal bonds and Treasury yields provide further context to this scene. The ratios of two-year, five-year, 10-year, and 30-year municipal bonds compared to their Treasury counterparts stood at 61%, 62%, 66%, and 82%, respectively. These figures, sourced from Refinitiv Municipal Market Data, indicate how municipal bonds are performing in relation to Treasuries, affirming the appeal of municipal securities in a challenged yield environment.

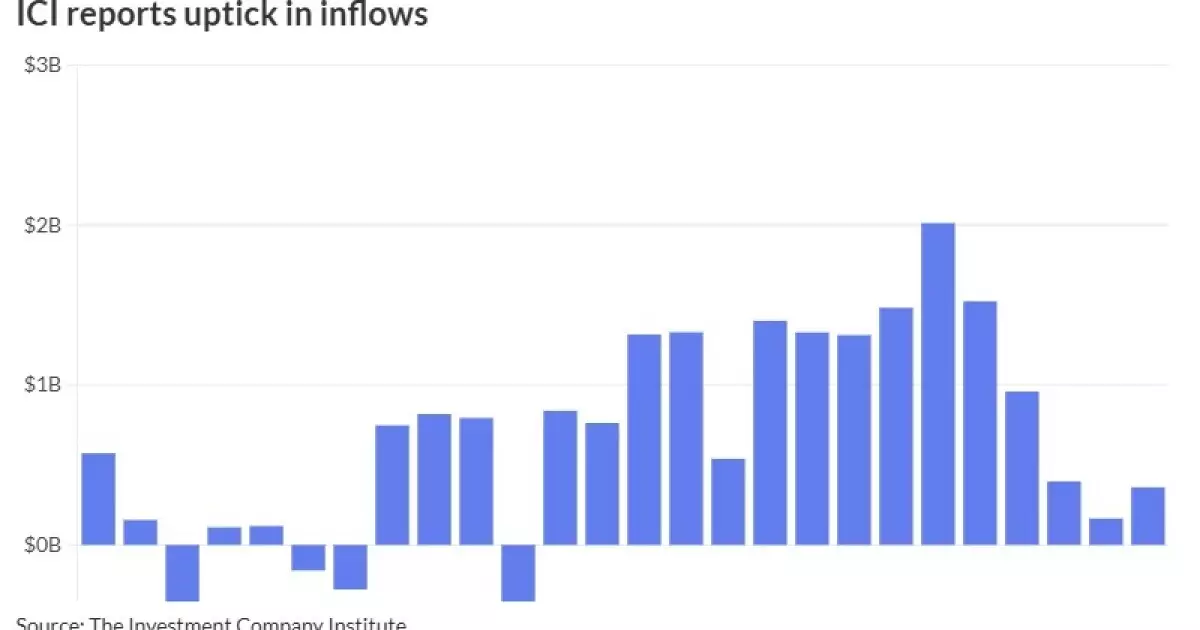

The municipal bond market is garnering solid inflows, indicative of increasing investor confidence. The Investment Company Institute’s report detailing a $360 million inflow into municipal bond mutual funds marks the 14th consecutive week of positive inflows, reinforcing the notion that investors are actively seeking the perceived safety of municipal securities. Conversely, exchange-traded funds (ETFs) did not fare as well, showing a significant drop in inflows this week, which might suggest a cautious approach by investors towards more liquid forms of municipal investments.

Moreover, the performance of municipal bonds stands in stark contrast to their Treasury counterparts. November has seen investment-grade munis delivering a solid 0.81% return, significantly outpacing the negative performance of USTs at -0.40% during the same period. Year-to-date, municipal bonds have generated a 1.63% return compared to the 0.96% return of U.S. Treasuries. This discrepancy in performance further solidifies the municipal market as a go-to asset class during uncertain economic conditions.

The Hunt for Yield Drives Municipal Market Activity

The current market scenario highlights a growing trend: the “hunt for yield.” Investors are increasingly gravitating toward higher-yielding municipal bonds as they seek avenues for better returns. Noteworthy market strategist Kim Olsan points out that high-yield municipal space remains attractive, with bond buyers continuing to make outright purchases, solidifying their commitment to the sector.

For example, recent offerings, like the Houston Airport’s 5% coupon bonds maturing in 2039 at a yield of 4.66%, illustrate the sound investment potential relative to other investment vehicles. Comparative assessments reveal that the taxable equivalent yield for these bonds can be enticing for a corporate buyer, further enticing investors who are navigating the current yield landscape.

This appetite is not restricted to new issuances; seasoned municipal securities are also drawing interest from investors looking to diversify their portfolios. The long-term benefits of municipal bonds, particularly in areas like essential services and general obligation bonds, continue to attract buyers in search of stability amidst turbulence.

The primary market for municipal bonds has remained active, evidenced by several recent issuances from varying states and sectors. For instance, Goldman Sachs recently priced $606 million in tax obligation bonds for Connecticut, demonstrating solid demand within the infrastructure category. This robust activity is mirrored by other notable issuers, including airport authorities and housing finance agencies, which are all tapping into investor sentiment favoring long-term municipal debt.

The yields from these offerings, alongside their associated credit ratings, further inform investors on the viability and potential risk associated with such bonds. For instance, the effective yields being offered on bonds from the Omaha Airport Authority and Pennsylvania Housing Finance Agency indicate a balanced risk-reward scenario, appealing especially to discerning investors.

As the investment landscape evolves, the outlook for municipal bonds appears optimistic. While there are challenges ahead, including economic uncertainties impacting revenues and the potential for governmental budget limitations, the ongoing influx of capital into the sector showcases its resilience. Continued investor interest underscores the importance of municipal bonds as a flexible investment option, capable of delivering returns even in a fluctuating market.

The municipal bond market’s current state reveals a complex interplay of investment strategies and performance metrics. With sustained inflows, stable yield ratios, and a vibrant primary market, municipal bonds remain an attractive investment avenue for those seeking safety and yield in a multifaceted economic environment. As investors continue the search for advantageous opportunities, municipal bonds are likely to stay a focal point in portfolios navigating uncertainty.

Leave a Reply