As the landscape of municipal bonds evolves, recent market activities reveal a subtle but significant stability in pricing despite rising U.S. Treasury yields. The day in review saw little alteration in municipal bond prices, indicative of steady demand as mutual funds continued to experience noteworthy inflows. This interplay occurs amidst an environment where U.S. Treasury securities faced upward pressure in yields, leading to a negative close on equity markets.

High-grade municipal bonds are garnering attention as the yield ratios indicate a robust 62% for two-year bonds compared to UST, trending comfortably above 60%. Ongoing investments within the municipal sector suggest that while short-term pressures exist due to federal yield adjustments, investor confidence remains resilient, particularly for tax-exempt instruments.

Delving deeper into the metrics, the reported ratios reflect a generally favorable environment for municipal bonds. Wednesday’s figures articulated a two-year yield at 62%, escalating slightly through the yield curve to 85% for longer durations. Expert insights from Kim Olsan, an experienced fixed income portfolio manager, highlighted that the current dynamics have not dramatically altered the yield range despite recent fluctuations in UST.

This stable performance is significant, especially since the 10-year MMD yield remains fairly close to its annual average of 2.75%. However, the 30-year segment of the market may need to see an increase of approximately 20 basis points to reach its average yield of 3.72%. Such conditions present a dual narrative of potential opportunity while underlying certain constraints, particularly for long-term bonds that have struggled to gain additional traction in performance metrics.

Enhancements in secondary market flows indicate a shift toward longer maturities, which have illustrated a sharp increase in traded volume among tax-exempt instruments, capturing 55% of total transactions. This observed shift towards longer bonds could imply that investors are seeking out improved yield differentials, potentially to hedge against the volatility present in the market.

Olsan notes that high-quality municipal names are particularly appealing, with offerings from state GOs yielding enticing returns that draw buyers eager for security and competitive yield enhancements. Discussing recent trades, specific Ohio GOs at 3.61% present about 60 basis points of additional yield compared to their shorter counterparts, embodying the tactical strategies employed by investors.

The primary market landscape has seen notable modifications as issuers adjust their offerings in response to strong investor interest. For instance, significant adjustments in deal sizes exemplify the uptick in demand; the South Carolina Public Service Authority’s deal surged to $1 billion from an initially intended $650 million, signaling optimism in municipal credit attractiveness. Similarly, the New York City Municipal Water Finance Authority’s increase further emphasizes the underlying appetite for long-term municipal commitments.

Furthermore, structured deals with appealing coupon rates are showing positive demand, with bonds designed to yield competitive returns appealing to diverse buyer profiles, including institutional and corporate applicants. Olsan’s emphasis on “heightened volatility” paints a picture of a cautiously optimistic market environment where certain maturities may provide strategic investment opportunities in the near term.

Geographically, supplies project across various states yield contrasting market sentiment. New York appears to grapple with a substantial estimated negative balance, which could heighten competition among in-state buyers in the upcoming weeks. Conversely, states like Pennsylvania are anticipated to experience a positive net supply, suggesting widening spreads within certain state GOs.

Demand for tax-exempt issues within these regions remains anchored by the intrinsic value of state-specific exemptions. As the market accommodates shifting supply and redemption patterns, pricing dynamics are likely to reflect these regional variations – with stretched spreads particularly pronounced where liquidity is tight.

Overall, the interplay between local and national levels underscores the complexity of municipal investing. Factors such as state financial health, demand for local bonds, and the evolving national yield curves collectively shape the investment milieu, ensuring that investors must remain vigilant and adaptable.

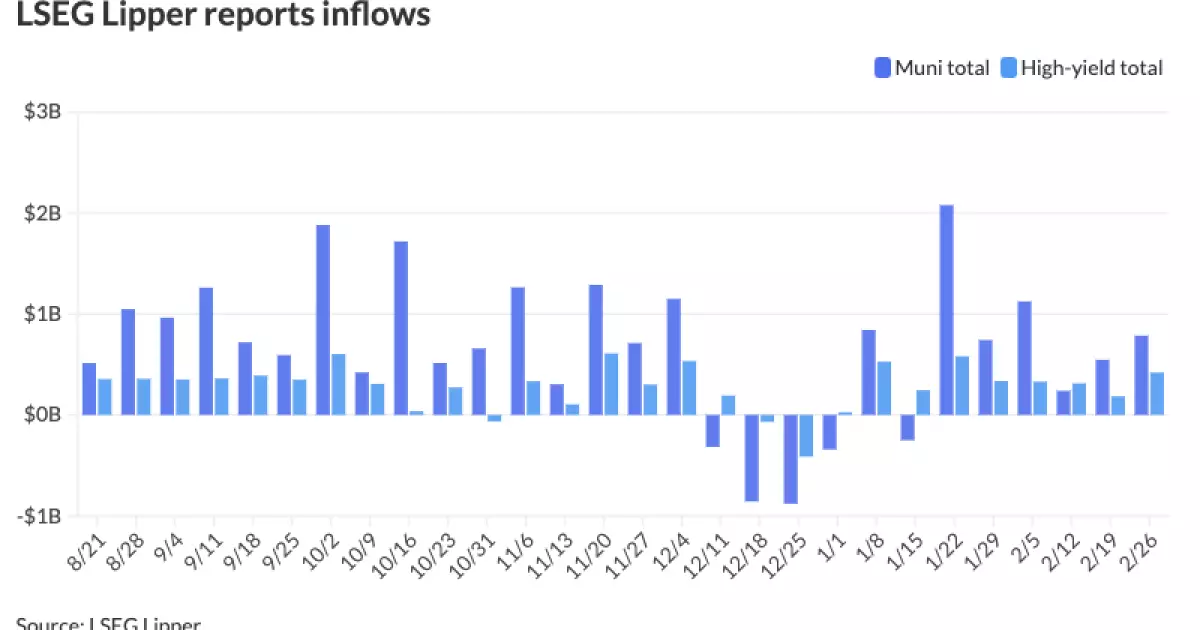

Investor activity reflects an increasing trend toward municipal bond funds, with record inflows recently reported, drawing interest worth $785.5 million in a single week. The continued preference for high-yield municipal funds positions them favorably amid tepid tax-exempt money market fund performances contrasted with substantial pullbacks on taxable funds.

As the market anticipates the March issuance and redemption cycle, prospects for strategic investments may reveal themselves, albeit with some variability in demand across different municipalities. As each state grapples with its idiosyncratic fiscal landscapes, investors would benefit from a nuanced approach that accounts for broader economic signals as well as localized supply challenges.

Navigating this multifaceted market narrative will require precision in analysis and a keen understanding of the evolving dynamics that govern municipal bonds, opening pathways for innovation and opportunity in a traditionally stable asset class.

Leave a Reply