The recent clamor around municipal bonds being a “safe haven” in a shaky economic environment needs a more skeptical eye. Yes, the muni market has exhibited modest gains and steady inflows, but to interpret this as a sign of true strength is to ignore the nuanced undercurrents coursing beneath its calm surface. While traditional narratives focus on incremental yield changes and stable demand, the reality presents a market strained by a lack of clear catalysts and structural weaknesses. This is not just a minor market hiccup; it’s a reflection of deeper systemic issues that threaten the sustainability of munis as a reliable asset class.

Why Yield Ratios Show a Market That’s Cheap But Not Irresistible

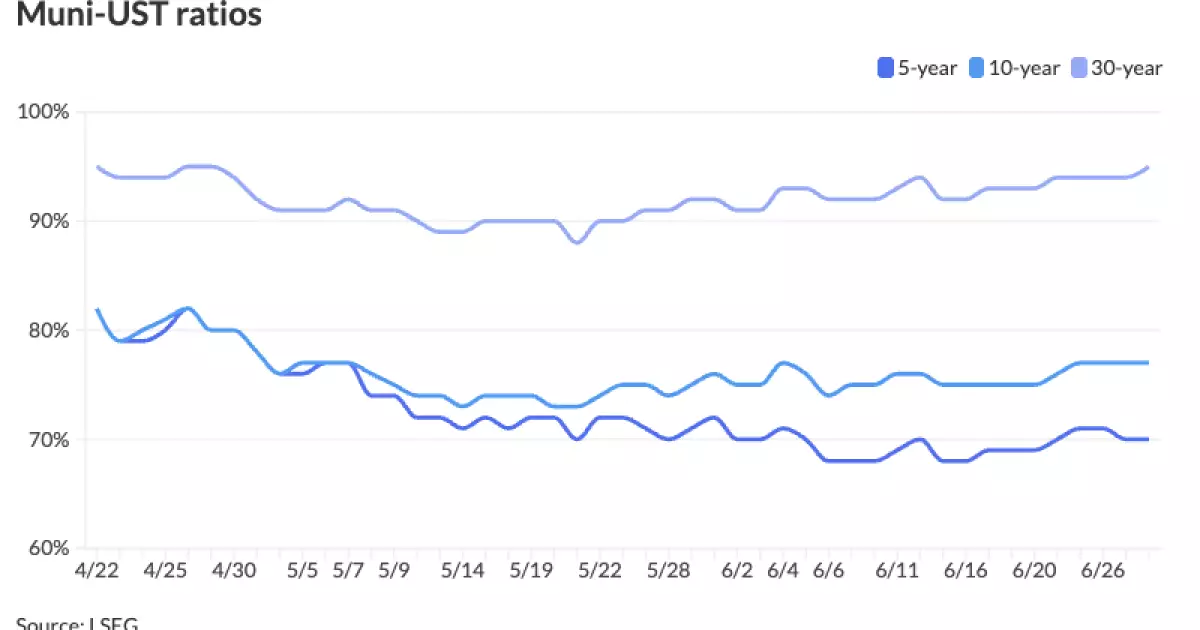

Municipal bond yields remain low relative to U.S. Treasury yields, with the two-year muni-to-UST ratio around 69% and the 30-year near 95%. On the surface, these depressed ratios suggest that munis are undervalued and present an opportunity for yield-starved investors. However, the value implied by these ratios is deceptive. The market participants themselves appear apprehensive, struggling to identify any meaningful catalyst that could spur these bonds to outperform. Without enough positive momentum—especially in fund flows—muni investors may find themselves trapped in a market that is “cheap” but lacks the dynamism to reward patience substantially. This stagnation is the intrinsic danger: the market looks attractive only because of a compressed baseline rather than genuine confidence in future returns.

Limited Volatility Masks the Lack of Genuine Momentum

The data shows “limited volatility and price movements” with muni yields fluctuating marginally, mostly flat in longer maturities. While some see this as stability, it’s arguably the opposite—a symptom of a market sidelined by uncertainty. Dealers report strong inquiries for attractively priced deals, yet cautious sentiment prevails. If investors were truly confident, one would expect a broader range of price action and more aggressive positioning. The subdued movements indicate a wait-and-see approach, reinforcing the idea that despite generous yield spreads—some high-grade bonds pricing above 8% after tax—investors hesitate to commit fully due to macroeconomic uncertainties and political risks looming on the horizon.

Fund Flows: A Slow Burn That’s Hardly Convincing

After nine consecutive weeks of positive inflows into municipal mutual funds, the absolute amount—$76.9 million—is underwhelming relative to the enormous scale of the market. For a sector that has been grappling with the aftermath of significant sell-offs earlier this year, these inflows are marginal at best and unlikely to generate the surge in demand necessary to prompt outperformance. The sluggish pace of fund flows underscores structural investor skepticism, possibly tied to concerns about rising interest rates, inflation pressures, and state fiscal health. In a genuine bull market, one would see far more robust and decisive capital influx rather than these slow, cautious gains.

The Primary Market: A Double-Edged Sword of Generous Spreads and Limited Issuance

Dealers praise the primary market’s resilience, noting that new issues attract strong subscriptions and favorable pricing. Yet this apparent strength masks a troubling fact: primary issuance is restrained, especially as we approach quieter weeks with holidays and reduced activity. For instance, states like California and New York will see sizeable bond redemptions—$5.4 billion and $4.4 billion respectively—but new bond issuance remains limited, with no state expected to exceed $1 billion in debt issuance in the short term. This mismatch creates a technical imbalance where the market’s ability to absorb new supply without disrupting yields is being tested. If issuance picks up amid less enthusiastic demand, prices could quickly reverse, sidelining investors who have grown complacent.

The Political Backdrop: Fiscal Headwinds You Can’t Ignore

Municipal bonds cannot be divorced from the political reality facing U.S. state and local governments. Rising inflation costs, contentious budget battles, and shifting federal support cast a shadow over many issuers’ creditworthiness. Investors are increasingly aware that some states, despite rating agency affirmations, carry hidden fiscal vulnerabilities that could worsen should economic conditions deteriorate or political gridlock persist. Unlike corporates or Treasuries, munis depend heavily on the local political will and tax base stability—factors that are not easily predictable and remain highly sensitive to changes in governance. The Minnesota or Illinois of the future might not look like their benign present, and such risks are not fully priced into current muni valuations.

Looking Ahead: Why Caution, Not Optimism, Should Prevail

The upcoming weeks promise plenty of action with large deals from the California Community Choice Financing Authority, New York State Thruway Authority, and various transportation entities. While these deals might momentarily create buzz, they also increase supply against a backdrop of tepid demand. Investors should prepare for potential price pressure, especially as reinvestment cash floods the market. The cycle of redemption and issuance could amplify volatility rather than reinforce stability.

Moreover, the remarkable resilience of the municipal market to date owes much to an extended period of supportive monetary policy and benign macro conditions. With the Federal Reserve’s tightening stance continuing and inflationary pressures persisting, the muni market’s fate is delicately balanced between technical support and fundamental risks. This precarious equilibrium means that only investors with a deep understanding of individual credits and a clear tolerance for uncertainty should venture into this market now.

In essence, municipal bonds today are less a fortress of safety and more a house of cards tempting yield seekers with their apparently attractive spreads. The cautious center-right investor should recognize the red flags and approach muni investments with vigilance, focusing on credit quality and state-level fiscal health rather than chasing yield in what could be a false rally.

Leave a Reply