The current landscape of municipal bond issuance presents a paradox that demands scrutiny. On the surface, it appears to be an inflow of capital reflecting economic optimism—issuers racing to capitalize on favorable market conditions, driven by fears of potential policy changes and volatility. However, beneath this veneer lies a complex matrix of strategic behavior, market vulnerabilities, and potential systemic risks that could unsettle the very foundations of municipal finance.

The relentless pace of issuance, peaking at record levels, signals a market eager to lock in low rates and extend debt maturities. Yet, this urgency may also be a defensive maneuver, a preemptive response to uncertainties around federal fiscal policy, tax law changes, and geopolitical shifts. Governments and private institutions are frontloading debt, risking a future landscape where heavy refinancing obligations or market saturation could trigger instability. This pattern is reminiscent of a house built on quicksand—appearing strong but vulnerable if the tide of market conditions recedes.

Furthermore, the segment’s resilience amidst volatility, such as the April tariff-induced pauses, raises questions about the true strength of investor confidence. The dominant retail investor base, often characterized as conservative, has shown little sign of panic or retreat, which is positive in the short term. But is this complacency sustainable in the face of mounting debt levels? Or is it merely a testament to the current interest rate environment—bolstered by the higher yield spreads—that temporarily masks deeper vulnerabilities?

The Role of Policy & Politics: Shield or Sword in the Municipal Market?

Political developments continually shape the municipal bond landscape. The specter of tax exemption reforms has historically loomed over the market—yet, year after year, they are either mitigated or postponed, fostering a false sense of security. The recent legislative standoff, where key exemptions like private-activity bonds remained untouched, has provided temporary reassurance. But this is a fragile appeasement; political tides can change swiftly, and the risk of targeted tax policy adjustments lurks beneath the calm.

A less obvious but equally profound influence stems from the actions of elite institutions—prestigious universities and large municipalities—who are capitalizing on their strong credit profiles to aggressively expand their borrowing. This elite-driven debt binge can distort market signals, artificially inflating demand for municipal bonds and creating a skewed perception of market health. It raises concerns about whether the broader market is sustainable when heavily concentrated among select high-credit issuers, leaving vulnerable smaller entities potentially exposed to future shocks.

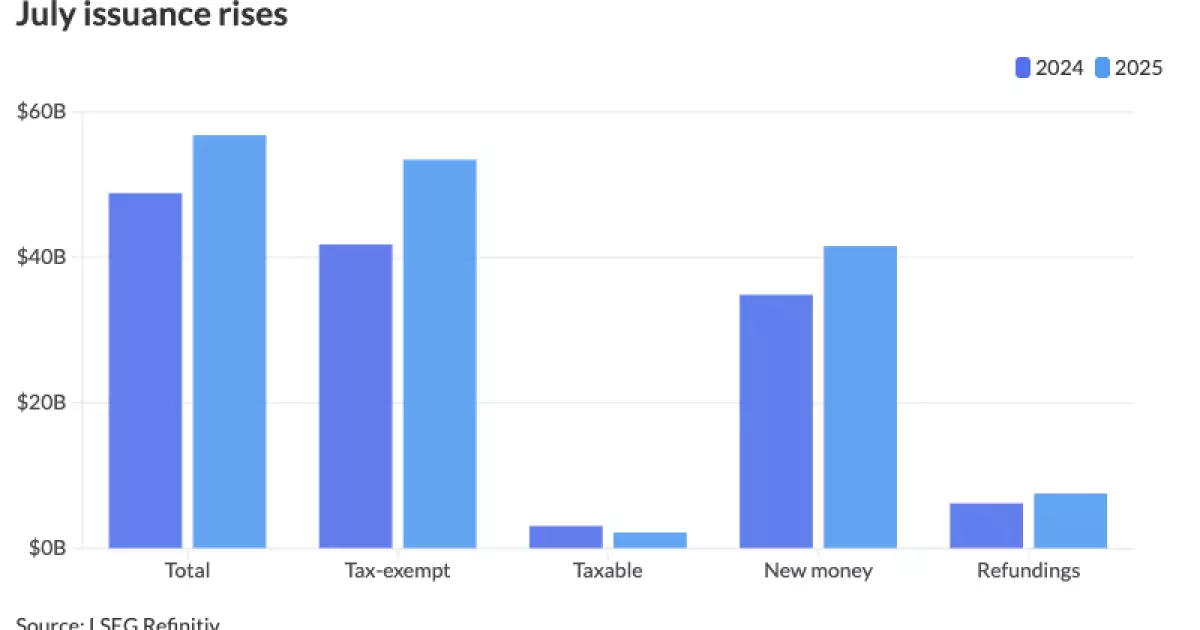

Meanwhile, the government’s fiscal stance, with increased issuance at the state and local levels, might simulate stability but risks embedding long-term liabilities that could burden future taxpayers. The surge in new money issuance—nearly 20% higher than last year—paints a picture of active, possibly over-leveraged, governments betting on continued fiscal health. Is this prudent stewardship, or gambling with future fiscal flexibility?

The Market’s Fragile Optimism: A Double-Edged Sword

The increase in issuance projections—from estimates of around $500 billion to upwards of $600 billion—reflects widespread optimism about the municipal market’s resilience. Yet, such rapid growth can be a double-edged sword. Excessive supply, if not matched by sustained demand, threatens to dilute liquidity and inflate borrowing costs. While current spreads are attractive, particularly in high-yield sectors, they could evaporate quickly if investor sentiment shifts or economic fundamentals weaken.

Moreover, the recent adjustments by major forecasting entities indicate a belief that the market’s growth is sustainable—yet, history has shown that rapid expansions often precede downturns. When the market reaches such levels, even minor shocks—be it a rise in interest rates, a geopolitical event, or political meddling—could trigger a sharp correction. The danger lies in complacency; investors and issuers alike might assume that the current robust trend implies perpetual growth, ignoring the inherent cycles within capital markets.

Despite the apparent strength, some sectors—like the distressed Affordable Housing or underfunded pension obligations—still harbor latent risks that could erupt if market dynamics turn sour. The very fact that some states and sectors have shown significant growth (e.g., California’s hefty issuance, up nearly 26%) could exacerbate regional imbalances, creating pockets of overleveraging that threaten broader market stability.

Market Adaptation or Overconfidence? A Crucial Crossroad

Financial markets are known for their adaptability, but there is a real danger of overconfidence in the municipal bond space. The steady influx of capital and high issuance volumes may fuel a narrative of perpetual optimism—yet this narrative can be dangerous. When markets operate at high capacity, the margin for error narrows, and the slightest miscalculation could snowball into broader financial disturbances.

The rising demand for tax-exempt bonds in a higher interest rate environment is particularly notable. While current yields offer a compelling reason for issuance, they might also create a bubble-like scenario where the perceived safety of municipal bonds is overestimated. The historic low default rates are reassuring, but they do not guarantee immunity from future shocks—especially if cumulative debt burdens become unsustainable or if overly optimistic project forecasts fail to materialize.

Additionally, the heavy focus on state-level issuance, with California leading, could mask underlying regional disparities. States with aggressive borrowing policies may appear robust today, but their long-term fiscal resilience is questionable, particularly if economic growth stalls or fiscal policies tighten. This divergence between short-term market exuberance and long-term fiscal prudence underscores the importance of vigilance and skepticism in assessing municipal finance health.

Finally, the sheer scale of recent issuance raises concerns about market capacity. Can investor appetite be sustained when supply continues to climb? And will the market remain resilient if macroeconomic conditions unexpectedly sour? If history is any guide, complacency in such an overheated environment could be the recipe for future instability—a risk that central planners, investors, and policymakers should not dismiss lightly.

Leave a Reply