The recent fluctuations in the municipal bond market seem to dance on the edge of stability, leaving investors unsure whether they are witnessing resilience or the first signs of fragility. Despite seemingly positive indicators—such as a strong support from Treasury market strength and persistent reinvestment flows—the underlying currents suggest a much more complex situation. The market’s whisper is that what appears to be strength is often a veneer, masking vulnerabilities that could surface as early as next month. While many cheer the $55 billion reinvestment flows entering the market, a critical analysis reveals that this influx might merely serve as a temporary patch rather than a sustainable foundation.

The “strength” attributed to the municipal bond sector is primarily driven by elevated issuance and the not-so-silently looming threat of rising interest rates. The steady decline in Treasury yields offers a temporary reprieve, but it masks the specter of longer-term market destabilization. An overreliance on short-term inflows and reinvestments can lull investors into a false sense of security. In the grand scheme, it is essential to recognize that beneath the apparent stability lies an increasingly steep yield curve that could herald volatility if conditions shift unexpectedly.

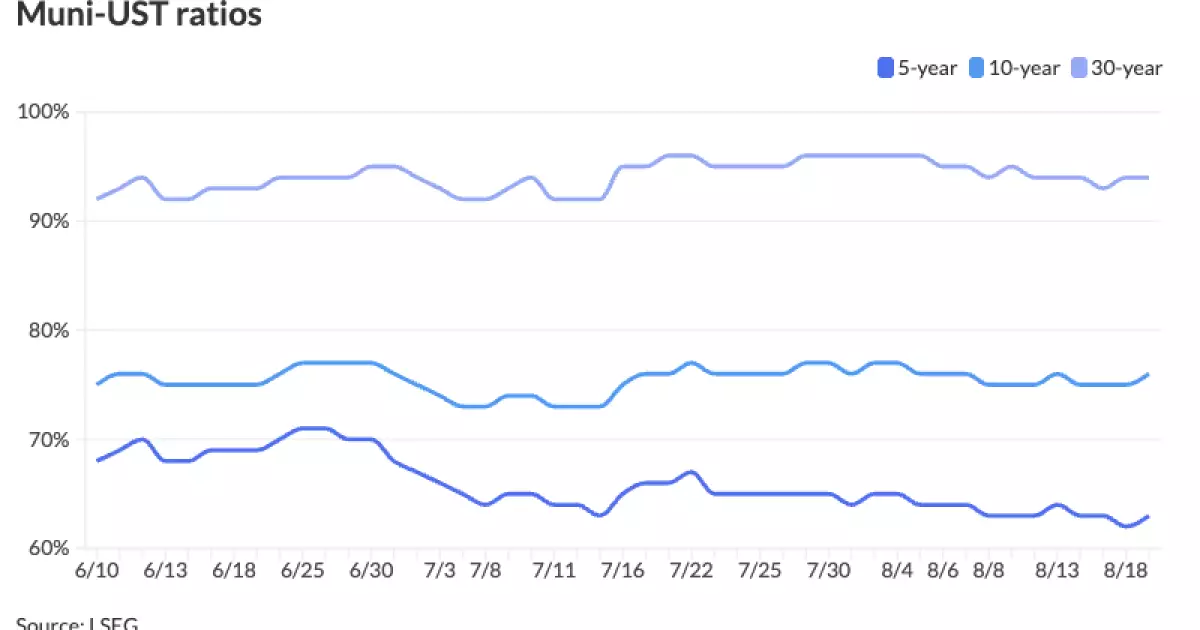

Analyzing the Yield Curve: Steep Slopes and Hidden Risks

The steepening of the yield curve has been a defining feature of the municipal landscape lately. While higher yields attract investors seeking income, this phenomenon also signals underlying concerns about credit risk and economic stability. The widening spreads, especially in the longer maturities, point to a disconnect—where risk premiums are swelling, and investor confidence may soon be tested.

What is particularly unsettling is the disparity between widening credit spreads and the relatively stable term spreads. This divergence hints at a market that is heavily bid and willing to accept risks that should, in theory, command higher returns. However, this scenario cannot last indefinitely. The elevated spreads could become a ticking time bomb if credit deterioration accelerates, especially among lower-rated borrowers. The confidence in these risk premiums may be misplaced; the current “cheap” long-term borrowing costs are likely masking vulnerabilities that could erupt under stress.

Furthermore, the notion that wider curves will persist is overly optimistic. As reinvestment flows decrease and issuance potentially normalizes, investors could find themselves caught in a liquidity squeeze. The period from September to June 2026 may reveal not just a fall in reinvestment but also an increase in maturities maturing into a less accommodating market environment.

Supply Dynamics and Their Long-Term Implications

Despite expectations that issuance levels might decline from the record $366 billion in 2023, the reality is far more complex. Elevated issuance still lingers, and while September’s scheduled total is modest relative to recent months, the infrastructure for continued high issuance remains. The current pace suggests that the market is prepared to absorb large volumes of new debt, but only at the cost of increasing systemic risk.

The concern is that this high issuance stokes a cycle of dependency. Municipal entities are borrowing at historically low rates, which sounds attractive until the realization dawns that many of these projects and refinancings might come with over-leverage. When combined with a possibly tightening monetary policy—especially if the Federal Reserve signals fewer or no interest rate cuts in 2025—the cost of issuance could unexpectedly shoot higher, diluting the attractiveness of municipal bonds and dampening demand.

This scenario underscores an important point: markets often behave in cycles, and the recent optimism could be a front for underlying structural weaknesses. The risk lies in the market’s blindness to the fact that a significant portion of issuance is built on a fragile foundation of low yields that masks deteriorating credit quality among some issuers.

Flow Patterns and Their Implications for Investors

Recent shifts in investor behavior reflect a broader uncertainty. While inflows into separately managed accounts have swelled, indirectly signaling retail demand remains solid, withdrawals or dips in non-exchange-traded fund flows suggest that investors are growing cautious. Inflation data and other macroeconomic indicators cast long shadows over the future of municipal fixed income.

The absence of contagion from recent headline risks should not lull investors into complacency. High-yield segments and vulnerable issuers—such as those involved in recent high-profile situations like Brightline—are beginning to show stress signals. These developments, coupled with the ongoing hurricane season, project a landscape where longer maturities and lower-rated borrowers could face additional pressure. The steep yield curve essentially becomes a mountain of potential pitfalls that could tumble if economic conditions deteriorate further.

The challenge for investors is discerning whether current demand, sustained by tax advantages and yield spreads, can endure the shifting macroeconomic backdrop. The looming possibility that the Federal Reserve’s stance could tighten further complicates this calculus. The only apparent safeguard appears to be the continued demand from income-focused investors willing to accept some negative total returns for the sake of yield—yet, this may not be sustainable if credit quality erodes more rapidly than anticipated.

Market Actors and Upcoming Catalysts

The upcoming primary market activities highlight the ongoing confidence in municipal debt despite wider economic tensions. States and municipalities are rushing to price billions in bonds—covering everything from school districts to health systems—emphasizing their reliance on favorable market conditions. However, these deals should not overshadow the broader risks that persistent issuance and challenging macro trends pose.

Institutional players like BofA Securities, RBC Capital Markets, and Barclays are active in pricing large deals, signaling continued institutional confidence—yet, their involvement shouldn’t be mistaken for immunity to potential shocks. The current fervor could mislead some into believing that municipal bonds are unbreakable, but prudent investors will recognize that market sentiment can shift quickly, especially if economic indicators tighten or if inflation fails to stay in check.

The market’s future hinges on pivotal data releases—such as Fed meeting minutes and inflation reports—that could alter the landscape overnight. If rate cuts don’t materialize as expected, the associated demand dynamics will shift, perhaps inadvertently exposing the underlying fragility of municipal finances. Yet, even with these risks, the defensive posture of most high-net-worth investors and the continued demand from tax-aware entities suggest that municipal bonds remain a central, albeit cautious, pillar of income-focused portfolios.

In conclusion, the municipal bond market currently embodies a paradox: robust demand and high issuance coexist with underlying structural vulnerabilities. What looks like strength in the short term could, in reality, be window dressing masking a more profound period of adjustment ahead. Savvy investors and policymakers need to look beyond the surface and prepare for the eventual realignment of yields, credit quality, and market confidence—facing the truth that not all that glitters in municipal markets is gold.

Leave a Reply