The municipal bond market has experienced a robust surge in weekly issuance over the past several months. This trend has been driven by pent-up capital needs, dwindling federal aid, and front-loaded issuance strategies adopted by state and local governments. Experts have revised their volume forecasts for 2024 upwards, with HilltopSecurities revising its issuance forecast to $480 billion due to stronger-than-expected economic growth. Similarly, Municipal Market Analytics now expects issuance to reach $475 billion to $500 billion based on the pattern observed in 2016.

Record-Breaking Numbers

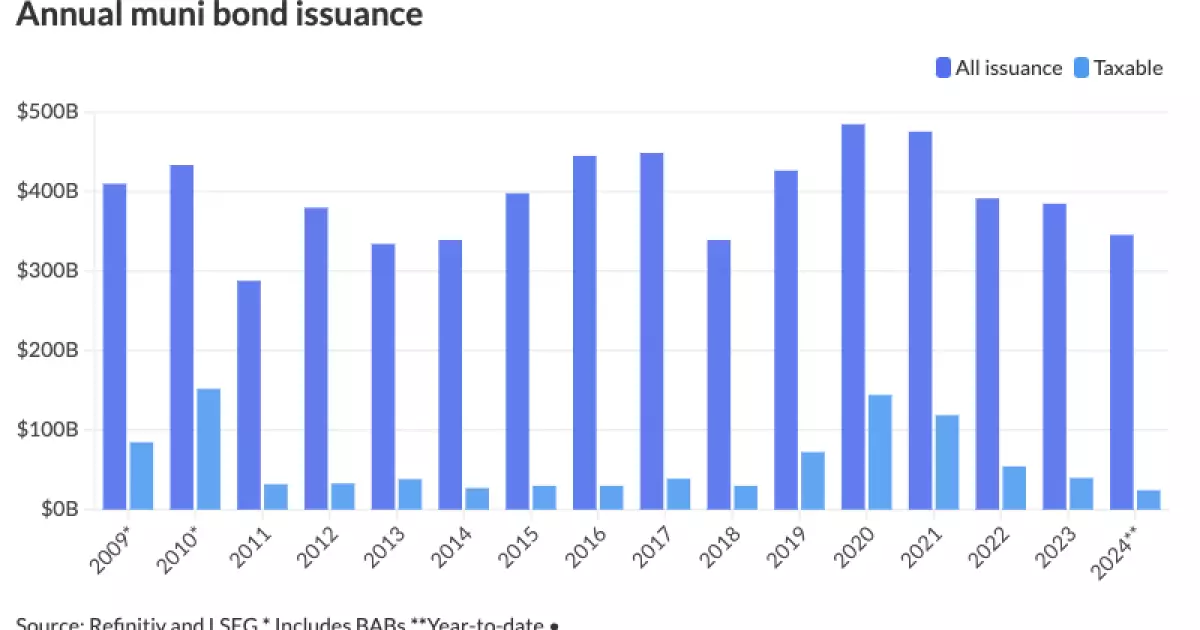

In 2020, the municipal bond market witnessed a record total issuance of $484.6 billion, followed by $483.234 billion in 2021. However, the past two years saw a decline in volume, with issuance dropping to $391.298 billion in 2022 and $384.715 billion in 2023. Despite these setbacks, 2024 is on track to surpass the previous all-time record of $448.6 billion set in 2017. As of Wednesday, issuance stands at $345.327 billion, marking a significant 32.7% increase over 2023.

The surge in issuance can be attributed to various factors, including the influx of new-issue calendars and the desire of issuers to come to market before the Federal Reserve meeting. Mega deals, such as those from Washington, D.C., the New York City Transitional Finance Agency, and Illinois, have contributed to the increased issuance volume. These deals offer something unique, and most large issuances occurred prior to key economic reports like the Consumer Price Index and Producer Price Index.

In the primary market, notable deals included GOs from Washington, D.C., tax-exempt bonds from the New York City Transitional Finance Authority, and GO refunding bonds from Illinois. The reception of these deals is viewed as a barometer of the overall muni market sentiment. Spreads on Illinois bonds compared to AAA yields indicate market expectations, with wider spreads anticipated due to the deal size and market conditions.

Despite a slight drop in The Bond Buyer 30-day visible calendar, the market anticipates continued issuance momentum. Issuers are keen to get ahead of potential market turbulence related to the upcoming election, as historical trends show a slowdown in issuance post-election. However, increased issuance may lead to a decrease in buy-side interest, as buyers become more cautious in their investment decisions.

The municipal bond market is witnessing a surge in issuance driven by various economic factors and market dynamics. The increased volume of issuance, coupled with revised forecasts and historical trends, paints a picture of a market that is responsive to external stimuli and evolving conditions. Issuers and investors alike will need to navigate this environment carefully to capitalize on opportunities and mitigate risks in the ever-changing landscape of municipal finance.

Leave a Reply