As of mid-week, municipal bonds have demonstrated slight softness while managing to outperform the pressures faced by U.S. Treasury securities. This resilience can be attributed to heightened investor interest in new issuances, which showcase significant demand, highlighting a market that is both active and competitive. In the realm of equities, a generally positive performance persisted, suggesting that investor sentiment remains cautiously optimistic despite broader market fluctuations.

The yield curve for triple-A rated municipal bonds saw minimal changes, with some segments deteriorating by one to four basis points. In contrast, U.S. Treasury bonds experienced more pronounced losses, particularly in longer maturities. Such discrepancies in performance are noteworthy, as they indicate a potential shift in investor preferences, particularly towards municipalities known for their relative safety and stable returns.

Recent figures reveal that the muni-to-Treasury yield ratios have adjusted downwards, reflecting shifting market dynamics. Such ratios are essential indicators, as they provide insight into the relative value of municipal bonds compared to government securities. For instance, the two-year municipal-to-Treasury ratio was reported at 63%, remaining consistent with prior readings, while the 30-year reached 84%, both according to Refinitiv Municipal Market Data. ICE Data Services provided similar ratios, further confirming the market’s stability.

This environment of declining ratios is compelling, especially considering the vast amounts of liquidity—reportedly over $6 trillion in money market funds and nearly $2.5 trillion in certificates of deposits. As rates begin to soften, many investors may divest from lower-yielding instruments and allocate their capital to longer-duration municipal bonds, which could offer compelling opportunities, especially for those seeking tax-adjusted returns.

Focusing on Federal Reserve policy, the tendency for “marginal” investors to shift towards longer-dated equities and munis is significant, particularly in light of potential rate cuts. The conjecture surrounding the Fed’s monetary policies always serves as a catalyst for investor behavior changes. According to Julio Bonilla, a fixed-income portfolio manager at Schroders, these shifts reflect a nuanced understanding of market trends and investor sentiment.

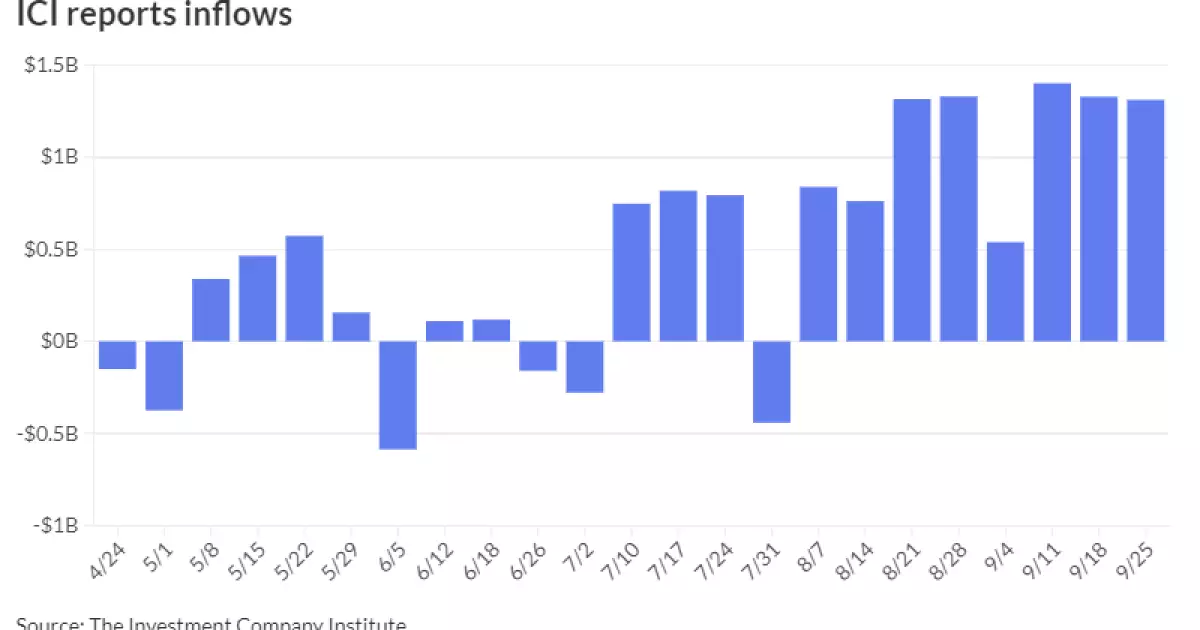

Moreover, the continuous flow of capital into municipal bond mutual funds reinforces this shift, with the Investment Company Institute reporting $1.312 billion in inflows within the last week. This suggests that retail investors are not just remaining active but are actively positioning themselves for anticipated changes in the market. The elevated activity in separately managed accounts, noted by experts, further underscores the importance of these funds in sustaining municipal bond performance amidst shifting demand dynamics.

Throughout the week, major issuers like Columbia University have tapped into the market with substantial offerings, including a noteworthy $500 million deal consisting of taxable corporate CUSIPs and revenue bonds. Such deals, characterized by their competitive spreads, point to both the demand from institutional buyers and the attractiveness of municipal bonds as viable investment vehicles. This trend is visible in the pricing of various bonds, including those issued by the Kentucky State Property and Buildings Commission and Massachusetts, which indicate healthy investor appetite.

The significant participation of institutional investors in primary offerings is crucial for the overall market environment. The success of these bond issuances signals confidence and can lead to increased levels of new financing in the near future. As such, we can expect that if the market rally continues, there could be an uptick in refunding activities, potentially pushing 2024 issuance levels to record highs.

Looking ahead, 2024 could present remarkable opportunities for issuers and investors alike. Should current trends of liquidity and favorable investor sentiment persist, municipalities may find themselves well-positioned to capitalize on lower borrowing costs. The cyclical nature of the municipal bond market often reflects broader economic conditions, and the current climate suggests an impending demand for municipal issuance.

Analysts keenly observe primary market performance as well as consumer behavior amidst these developments. If municipal bonds continue to attract retail investor interest and institutional participation, the market could foresee a vibrant year ahead, punctuated by strategic repositioning for long-term financial benefits.

The municipal bond market remains a fundamental segment of the broader fixed-income landscape. With current trends indicating robust demand, especially in a liquidity-rich environment, there exists a palpable optimism surrounding future performance. Investors are encouraged to remain vigilant, as potential fluctuations in Fed policies and economic indicators will undoubtedly impact this dynamic market.

Leave a Reply