The municipal bond market has demonstrated a notable resurgence lately, largely influenced by movements in U.S. Treasury yields and changes in fiscal policy expectations. On Monday, there was a tangible decline in municipal bond yields as market participants responded positively to the election of Donald Trump’s pick for U.S. Treasury Secretary. This article aims to dissect these trends, the factors contributing to them, and the implications for investors both in the short and long-term.

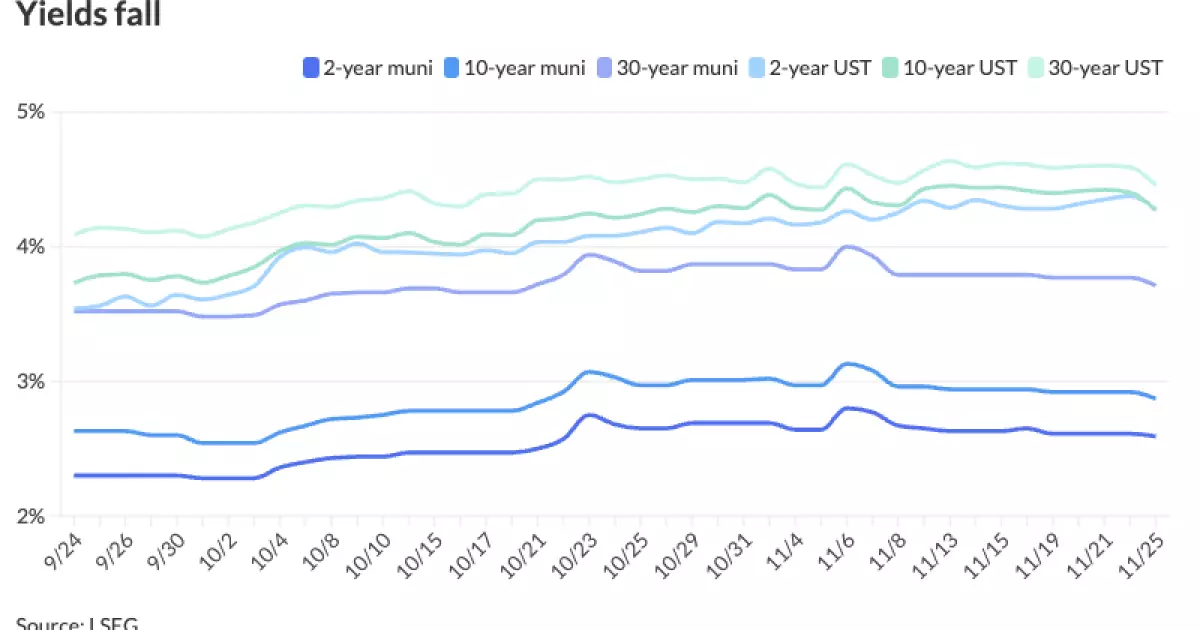

In a critical week for the municipal bond market, yields decreased by up to seven basis points, mirroring a rally in U.S. Treasuries. Specific movements showed USTs climbing as much as 15 basis points, which has been interpreted by analysts as a reflection of renewed confidence among investors. The financial community, reacting to the nomination of Scott Bessent as Treasury Secretary, seems to perceive this choice as a means to establish operational stability within a potentially tumultuous administrative context.

According to a UBS report, this perception of stability could recalibrate expectations regarding inflation and interest rates—often critical determinants of market behavior. The narrative suggests that, while the possibility of volatility remains, there is an emerging consensus that the overarching Trump administration policies may not prove as inflationary as once feared. In fact, UBS strategists project a likely decline in UST yields by 2025 after witnessing an upward movement of 65 basis points over the previous two months.

Despite facing significant challenges earlier in the year—with a reported 1.46% decline in October—municipals seem to have turned a corner. Recent figures indicate a turnaround, with returns showing a growth of 0.88% for the month of November to date. This resurgence has pushed year-to-date returns to approximately 1.69%, indicative of strong demand in the municipal bond sector.

As highlighted by Daryl Clements from AllianceBernstein, a marked appetite for tax-exempt income has been a major driver of this resurgence. The increasing attractiveness of munis, especially given the compression of after-tax spreads, suggests that investors are pivoting towards assets that provide steady income with favorable tax implications.

To understand the performance metrics more thoroughly, it’s important to examine the ratios of municipal to UST yields. Current data shows that the two-year municipal-to-UST ratio is at 61%, while the 30-year variant sits at 83%. These figures indicate that, particularly at longer durations, municipalities may appear relatively expensive compared to government bonds.

In terms of volatility, last week was particularly stable, marking a departure from the fluctuations observed earlier in the year. Birch Creek strategists noted that while yields experienced minor adjustments, they closely tracked movements in USTs, suggesting a synchronized market behavior. Investors are increasingly gravitating towards longer-dated and high-yield funds, which have become the focal point for inflows this year despite short-duration funds experiencing asset losses.

As the end of the year approaches, supply in the municipal market is expected to decrease, creating an intriguing dynamic. This week, the supply stands at a modest $1.4 billion, a drop that could indicate a tightening market environment. Notably, major upcoming issuances include several large deals that are poised to attract investor attention, such as the Greater Orlando Aviation Authority’s $843 million airport facilities revenue bonds and Hawaii’s $750 million taxable general obligations bonds.

Furthermore, with ongoing upgrades in credit ratings—such as a recent trio for various municipal authorities—there is potential for mounting investor interest, particularly in high-quality offerings. The calendar is expected to remain active, particularly in the first two weeks of December.

Overall, the municipal bond market is poised to navigate through a transformative period instigated by recent political and monetary developments. While the backdrop of U.S. Treasury yields and macroeconomic considerations will remain crucial, the adaptability of the municipal bond sector, evidenced by recent performance recoveries and strategic shifts, reinforces its ongoing appeal to investors. As we look to the year ahead, the trajectory of municipal bonds will depend significantly on external fiscal pressures and the evolving economic landscape, reinforcing the need for investors to remain vigilant and informed as they strategize their portfolios.

Leave a Reply