The current landscape surrounding municipal bonds is marked by a season that many traders and analysts refer to as “winter softness.” This term encapsulates the prevailing lack of momentum within the market, influenced by a confluence of factors such as diminishing new issuances and the plea of investors for stability amidst fluctuating economic indicators. It is vital to delve deeper into this phenomenon to understand its implications for the municipal bond market as we move into the new year.

As we approach the year’s end, the dynamics of the municipal bond market and the broader financial environment reveal a noticeable drop in investor activity. Jeff Timlin, a managing partner at Sage Advisory, provides critical insight into the temporary lull, pointing to the light staffing and decreased new issuance as primary hurdles impacting pricing guidance. The absence of substantial new offerings means that traditional price-setting mechanisms are now challenged, leading to thin market participation that can sometimes cause wider bid-ask spreads and increased volatility.

The notion of “tax-loss selling” as the year concludes carries weight as well. Investors often seek to realize capital losses to offset gains, influencing the liquidity and stability of the municipal bond market. It is during this intricate interplay of seasonal behavior and technical weakness that a somewhat contradictory picture emerges; while mutual funds continue to experience outflows, tax-exempt money market funds manage to attract significant inflows.

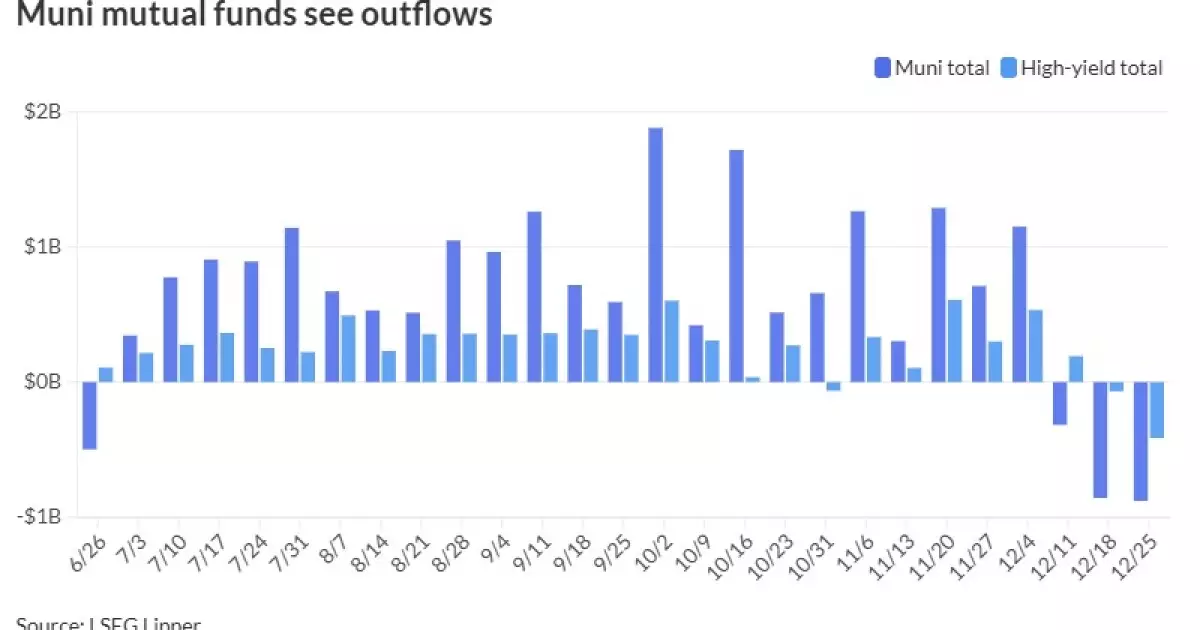

According to LSEG Lipper, significant outflows have been recorded in municipal bond mutual funds, with investors pulling a staggering $878.5 million for the week ending December 25. This figure was not isolated, following a previous week’s outflow of $859.6 million, showcasing a trend that investors should monitor closely. As high-yield funds similarly faced $413.6 million in outflows, it is apparent that the municipal bond space is witnessing a decisive shift in investor sentiment.

Interestingly, the Investment Company Institute’s data paints a somewhat different narrative, indicating a potential discrepancy in outflow reporting. While Lipper suggests a continuing trend of withdrawals, ICI reported a substantial inflow of $1.04 billion earlier in December. This divergence in reporting underscores the complexity and unpredictability of the current market environment — a landscape where capital allocation is increasingly selective.

While mutual funds appear to be struggling, the landscape for tax-exempt municipal money market funds is markedly more favorable. Recent data indicates inflows of $1.477 billion following the previous week’s outflows. This shift suggests that investors may be favoring the relative safety and liquidity of money market funds while remaining cautious about longer-duration municipal bond investments.

The average seven-day simple yield for tax-free and municipal money-market funds jumped to 3.08%, reflecting rising interest rates that have caught the attention of risk-averse investors. This change aligns with broader trends in taxable money funds that recorded substantial inflows this week, essentially accumulating over $53 billion.

The secondary market dynamics are crucial at this juncture. Timlin mentions that the issuance of new municipal bonds will typically stall until January, temporarily creating a market dependent primarily on existing secondary inventory. Therefore, during this period, dealers are less inclined to place aggressive bids, given the absence of new supply to integrate into the market. This could further complicate trading conditions as buyers and sellers navigate a limited supply situation until the new year.

Looking ahead, experts are optimistic about the return of a “wall of money” ready to re-engage with the market come January 2. With a potential issuance boom on the horizon, estimated at $500 billion or more, the market is poised for a revival. The influx of capital is expected to refresh municipal bond valuations, which have remained relatively stable despite current volatility.

Undoubtedly, the landscape of municipal bonds is intricate, marked by a clash of cautious investor sentiment and the underlying promise of a robust issuance environment in early 2025. Investors are likely to remain vigilant, navigating uncertainties while identifying opportunities amidst the swirling dynamics of supply and demand.

As we transition into the new year, the prospect of improved technicals and the enticing potential of abundant cash reserves lurking on the sidelines suggests that current inefficiencies may not persist. As Timlin accurately states, volatility should prove short-lived as investors deploy idle cash into munis, leading to a gradual shift toward more favorable valuations.

The interplay between market conditions, investor sentiment, and forthcoming risks will be paramount for municipal bonds. The anticipation surrounding January issuances, combined with the backdrop of holiday trading conditions, provides an intriguing yet complex evaluation for investors and analysts alike as we approach the dawn of a new financial year.

Leave a Reply