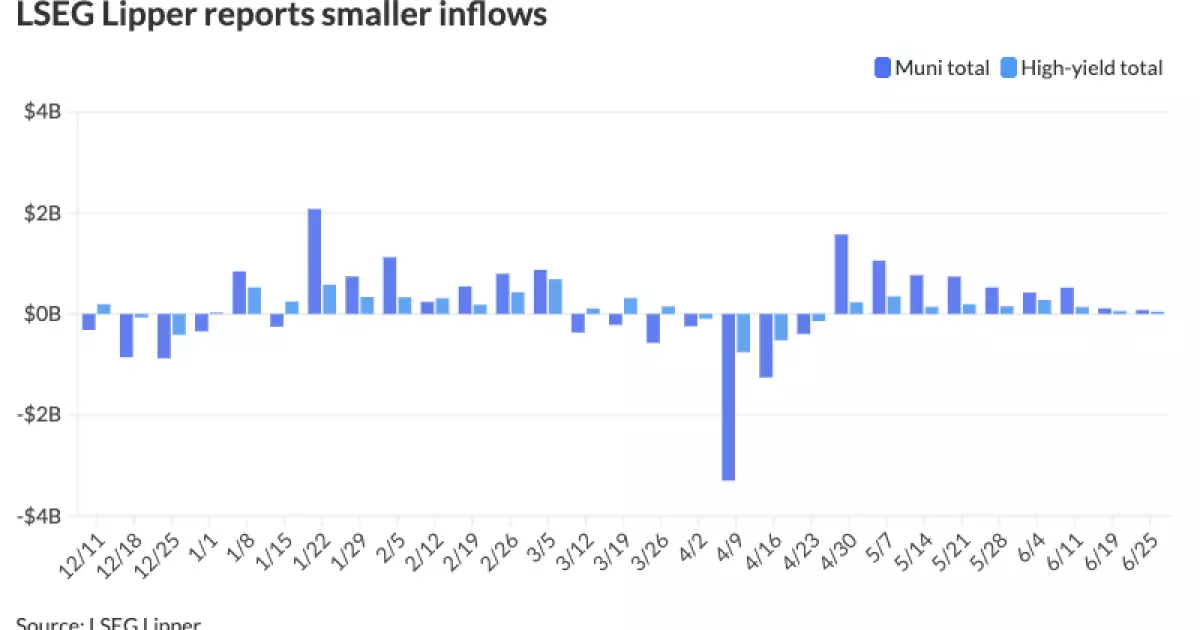

The municipal bond market, often seen as a steady harbor for conservative investors, is currently undergoing shifts that demand scrutiny. Recent observations indicated a notable resilience in the municipal sector as U.S. Treasury yields dropped, with the two-year municipal-UST ratio settling at a noteworthy 70%. Despite the lackluster performance in the year-to-date picture, where munis lag by a staggering 340 basis points behind Treasuries, there are signs of recovery amidst political and economic turbulence. As municipal bonds start to gain traction, one cannot help but question whether this recovery is sustainable or merely a fleeting moment of optimism.

Headwinds from political uncertainty have always pressured municipal bonds; however, recent clarity regarding legislative actions has contributed significantly to market stability. Investors are coming to terms with the implications of reduced federal support for local governments, which in turn may prompt a surge in issuances. The statistics are revealing: issuance among municipal bonds has surged by 16% relative to the previous year, with the first quarter alone recording the second-highest supply on record at $119.2 billion. This uptick in issuance reflects both necessity and opportunity as municipalities scramble to harness the capital markets for funding.

The Role of Interest Rate Volatility

The volatility of interest rates has profound implications for the municipal bond market. JB Golden, a well-respected executive director in the industry, has highlighted the impact of broad interest rate fluctuations, particularly at the longer end of the yield curve, on performance metrics. The latter half of this year may reveal whether munis can forge a path towards recovery, but investors are right to be cautious. A mere increase in demand does not equate to long-term stability or profitability.

Moreover, the recent trend of increased reinvestment demand signals a possible shift in sentiment, moving from headwinds to a potential tailwind for municipal bonds. The interesting interplay of reinvestment and issuance dynamics raises questions about whether municipalities can effectively manage the challenges posed by an overactive supply environment. It’s commendable that the market has exhibited resilience against substantial supply, digesting record amounts without succumbing to overwhelming pressure. However, one cannot ignore that each bond issuance comes with risk and responsibility, which is sometimes not viewed with the seriousness it deserves.

Demand and Valuation: Aligning Interests

The scenario in which valuations hit historically attractive levels sparks an intriguing dialogue. With munis finally appearing to attract investor interest after a period of stagnation, there exists an argument for their renewed appeal. However, one must remain skeptical about how long this upturn can be sustained amidst pressures such as inflation and ongoing fiscal uncertainty. While the valuations may suggest excitement, the crux lies in whether fundamentals can uphold this enthusiasm.

Institutional investors may be reluctantly eyeing the municipal sector as an alternative to Treasuries, which also exhibit their own sets of risks and uncertainties—especially with several economists projecting a potential downturn in the economy. The ongoing conversation about the relevance of municipal bonds often overlooks the inherent risks associated with increased market activity, which could lead to an appetite for higher yields but also invites the potential for losses in the event of market corrections.

Implications of Federal Policy on Local Governance

As municipal bonds grapple with the repercussions of federal policy changes, one must contemplate the long-term implications for local governance. With the continued reduction in federal support, municipalities are presented with a stark choice: become more self-sufficient or face fiscal distress. This paradigm shift raises concerns about both the quality of local services and the viability of long-term funding models. Greater reliance on capital markets to finance infrastructure and public services can lead to unmanageable debt levels if not approached judiciously.

Furthermore, as larger municipalities now issue record amounts of debt, the rift between economically prosperous locales and those struggling to maintain basic services continues to expand. If local governments become more competitive in the bond market, we may witness a flight of capital towards better-rated issuers, thereby accentuating the difficulties faced by struggling municipalities.

As the market transitions through the summer months, the potential for excess issuance juxtaposed with shifting investor sentiment could either reinvigorate or destabilize the municipal bond landscape. Will munis emerge as a trustworthy investment, or are we merely witnessing the calm before a storm? The coming months will undoubtedly paint a clearer picture, but one thing remains certain: vigilance and critical analysis remain essential in this continually evolving financial realm.

Leave a Reply