In the intricate world of municipal and Treasury bonds, market movements can often create ripples that affect investment strategies, yield rates, and overall market performance. Recently, the municipal bond market exhibited modest strength amid a backdrop of declining U.S. Treasury (UST) yields and a downturn in equities. This article endeavors to dissect the latest trends within this sector, focusing on yield ratios, performance metrics, issuance forecasts, and potential headwinds that could shape the landscape for 2024 and beyond.

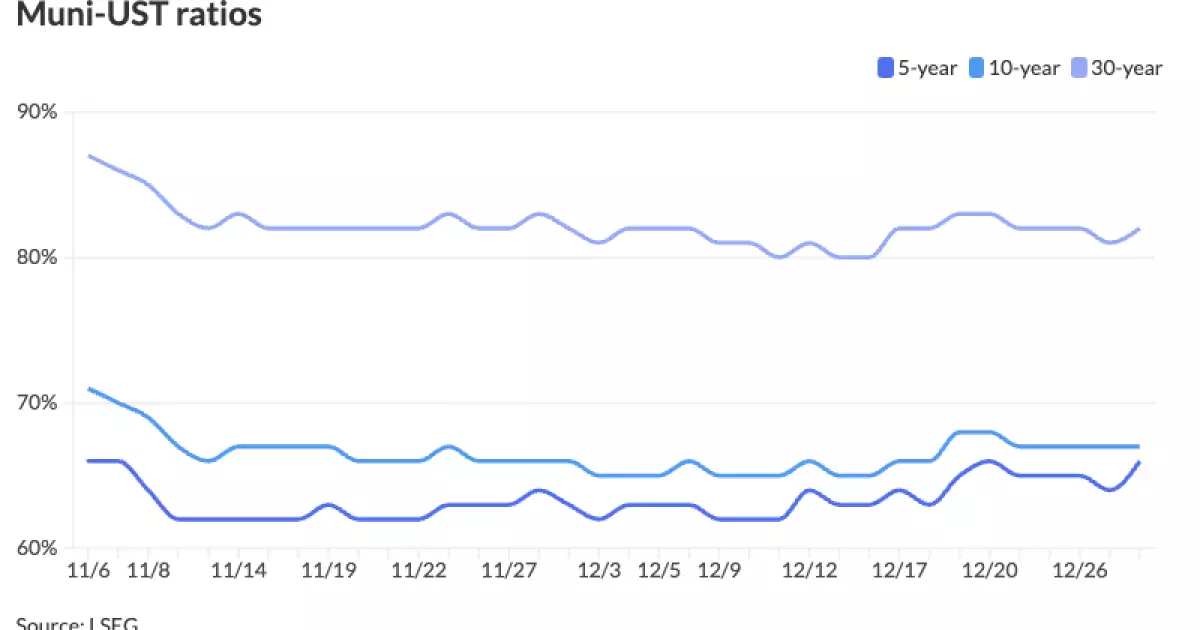

Recent data indicates that municipal bond yields have seen an increase of up to four basis points, while UST yields exhibited a more pronounced decline, dropping between five to nine basis points, especially in bonds maturing ten years and shorter. This divergence is illustrated by the ratios comparing municipal yields to UST yields: for the two-year and five-year maturities, the ratios stood at 66%, while the ten-year was at 67%, and the thirty-year was higher at 82%. This information, sourced from Municipal Market Data and ICE Data Services, underscores the performance of munis compared to their taxable counterparts, highlighting a year-to-date return of 0.73% for munis against 0.23% for USTs.

Despite this, it’s crucial to recognize that municipal bonds underperformed relative to USTs in the short term. Expectations for the coming year hinge significantly on the interest rate trajectory, as articulated by Barclays strategist Mikhail Foux. With premium investment-grade indices beginning 2024 at relatively high valuations—essentially without a safety buffer—Foux’s appraisal of the risk landscape proved insightful. The municipal market is indeed vulnerable to the pressures of a shifting interest rate environment.

The municipal bond market has experienced losses, notably a decline of 1.77% in December alone, although year-to-date metrics remained partially positive. In comparison, high-yield bonds also faced challenges, with a decrease of 1.97%, despite an impressive annual return of 5.98% thus far in 2024. Foux’s perspective suggests that high-yield spreads over USTs are sufficiently wide to offer attractive returns even amidst market volatility. However, the overall expectation is that both municipal and high-yield indices will likely finish the year richer than their UST counterparts, although this outcome leaves little room for comfort in the face of rate fluctuations.

Looking toward 2024, various factors could significantly influence the municipal bond space. According to Jeremy Holtz, a portfolio manager at Income Research + Management, the anticipated issuance of tax-exempt munis could range between $450 billion to $500 billion. This surge in supply may be propelled by the ongoing need for infrastructure upgrades and diminishing pandemic relief funds. There’s speculation about issuers potentially overloading the market to navigate changes related to tax exemptions,

Leave a Reply