The municipal bond market has experienced notable changes recently, characterized by rising interest rates and shifting investor preferences. A recent uptick in Treasury yields has influenced trading patterns, providing a backdrop against which municipal bonds are being traded. As investor sentiment fluctuates, market players are keenly observing how these macroeconomic shifts will influence bond pricing and demand, particularly as they approach the year-end period.

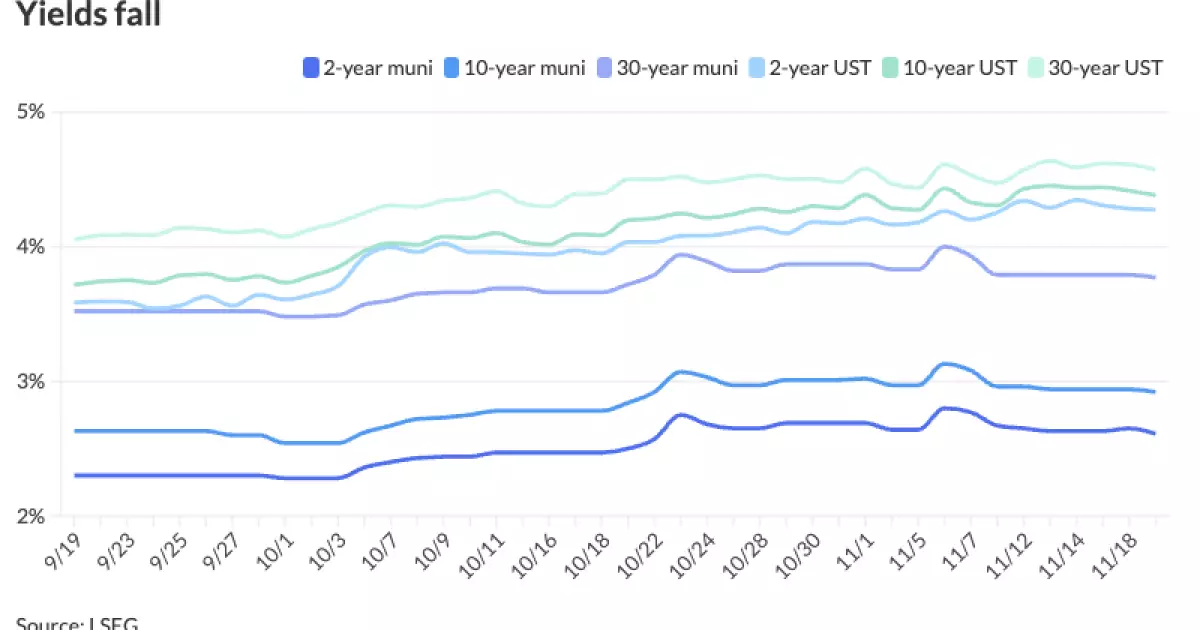

On a recent trading day, the yields on high-grade municipal bonds, particularly those rated Triple-A, decreased between one to six basis points across various maturities. This tightening of spreads relative to U.S. Treasury Bonds (USTs) suggests an ongoing resilience within the municipal market. While USTs exhibited modest gains, the municipal market’s continued outperformance reflects strong demand, especially in the longer-end maturities. Observing such a trend offers insights into the underlying strength of the municipal market, especially amid investor concerns related to inflation and credit risks that have been impacting USTs.

The decreasing ratio of municipal bonds to Treasuries—currently at strikingly low levels—highlights the desirability of tax-exempt income, particularly for retail investors seeking reliable returns. As observed, the ratios for the two-year, five-year, ten-year, and thirty-year benchmarks are impressively low at 61%, 63%, 67%, and 82%, respectively. These figures indicate a market that has become competitive and strategies geared towards ensuring more attractive yields are, thus, increasingly sought after by investors.

As the market shifts, the primary sector is seeing robust activity, led by significant issuances such as the $1 billion United Airlines Terminal project in Houston. This project reflects solid demand amid a broader market that is comparatively lighter than previous months, featuring notable deals that attract significant investor interest. Chris Brigati, a senior vice president at SWBC, emphasized that while the market is quieter than it was leading up to the election, strong underlying demand likely supports absorption rates for new issuances.

Alongside the primary market’s activity, other issuances in California for clean energy projects and transportation infrastructure bonds in Connecticut exemplify the growing appetite for socially responsible investment avenues, particularly green securities. The robust public interest in these bonds signifies a broader trend towards sustainability and fiscal responsibility in the municipal market.

Retail investor enthusiasm is becoming increasingly palpable in the face of rising yields, as they seek opportunities to enhance their income streams. The market has seen significant trade volumes—exceeding 300,000 transactions recently—underscoring a dynamic environment driven by both institutional and retail investor participation. Smaller transactions are garnering stronger buying conditions, as retail investors capitalize on the availability of favorable yields, further inflating demand.

Mutual funds, while demonstrating modest inflows, are rapidly evaluating how the overall demand landscape will evolve as 2023 approaches its close. The anticipation surrounding additional supply can potentially lead to enhanced trading conditions in the final quarter as well. The market is on track to witness an approximate $30 billion inflow by year-end, with historical comparisons showing only four superior years over the past fifteen years.

As we look towards the end of the year, paramount considerations emerge surrounding the anticipated supply of municipal bonds. If supply mimics last year’s trajectory—which showed a commendable $45 billion in issuances during a similar period—the municipal market could break the $500 billion mark in total supply for the year, indicating a stable performance environment.

Profitability in this landscape will hinge on UST yields maintaining their current levels without significant decline. Analysts suggest that minor price declines or yield hikes may be imperative for sustaining the anticipated inflow of bonds. With inflation fears casting shadows over credit conditions, cautious optimism is recommended for investors navigating this multi-faceted market.

In summation, the municipal bond market presents a complex interplay of performance, investor enthusiasm, and supply-demand dynamics. A resilient demand amid tightening spreads showcases the attractiveness of tax-exempt vehicles as strategies evolve in both the primary and secondary markets. The continued performance will primarily depend on external economic conditions and how investors respond to the ongoing challenges posed by inflationary pressures and shifting fiscal landscapes. Hence, stakeholders are encouraged to remain vigilant and flexible in their strategies as the year progresses toward its closing stages.

Leave a Reply