The municipal bond market is currently navigating a turbulent landscape marked by volatility, limited new issuances, and challenging market conditions. As December unfolds, investors are observing significant implications amid shifting U.S. Treasury (UST) yields and year-end positioning. The municipal bond sector’s performance, coupled with the trends observed in USTs, sets the stage for an analysis of the factors influencing municipal bonds as we approach the new year.

Recent Performance: The Impact of UST Losses

December has not been a favorable month for the municipal bond market, as it registered losses while being largely insulated from the declines in USTs. On a day when triple-A municipal yield curves remained stable, USTs experienced losses of up to six basis points, with the 10-year yielding over 4.6%. This divergence indicates a degree of resilience in the municipal space, even as the overall sentiment remains cautious, largely due to the implications of a volatile UST market.

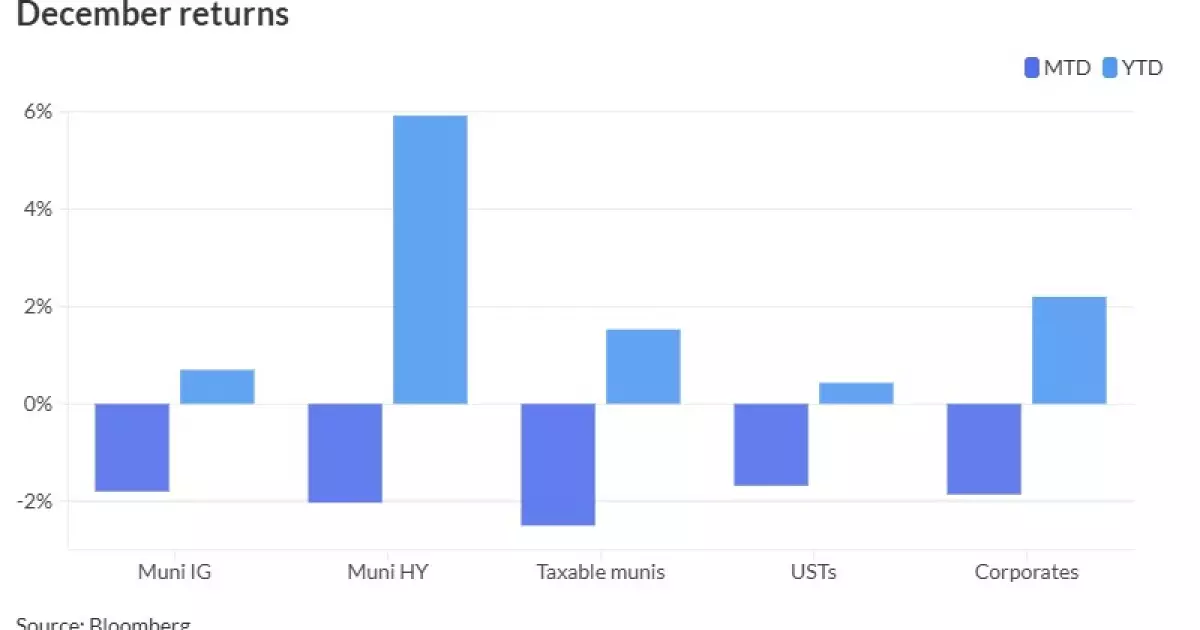

The Bloomberg Municipal Index reflects this sentiment, demonstrating a decline of 1.80% in December, against a modest year-to-date return of 0.70%. The high-yield segment shows a troubling performance of -2.03% this month, although it maintained a robust annual return of 5.92%. Taxable municipals also faced challenges, with a 2.50% loss in December while notching a 1.53% gain year-to-date. This multifaceted performance underlines the intricacies within the municipal bond market, especially in a year when external factors heavily influence investor behavior.

The upcoming weeks appear to hinge on the relationship between supply and demand. With net figures suggesting potential upward pressure, analysts highlight the importance of individual components such as separately managed account programs and exchange-traded funds. Kim Olsan, a senior fixed income portfolio manager, emphasizes the need for vigilance as new issuances remain sparse in the final week of December, which is traditionally free from significant new deals.

A notable aspect of this landscape is the disparity between expected supply and implied demand stemming from redemptions, which is projected at around $8 billion within the next 30 days—concurrent with the anticipated Federal Open Market Committee (FOMC) meeting. This conflicting dynamic raises potential concerns among investors about the broader implications on market liquidity and pricing stability, especially during a period characterized by fluctuating Treasury rates.

As the municipal market transitions into January, expectations shift with a flurry of anticipated new issuances across diverse sectors, including an impressive $1.05 billion of general obligation bonds from Washington State. Traditionally, January has been a robust month for municipal bonds, prompting some optimism; however, analysts remain cautious. Matthew Norton, the chief investment officer at AllianceBernstein, highlights potential challenges stemming from elevated supply levels and ongoing Treasury rate volatility.

These upcoming dynamics indicate that while January could herald stronger issuance volumes, the simultaneous presence of fluctuating interest rates may lead to investor hesitancy, impacting fund flows and market stability. The uncertainty regarding prospective tax reforms and legislative actions further complicates the issuance narrative, reinforcing the need for strategic foresight.

In 2024, lower-rated municipal credits are expected to continue outperforming higher-rated counterparts, challenging conventional assumptions about credit quality dynamics. Olsan draws attention to the trends observed in yield spreads between A-rated and AAA-rated bonds, observing that spreads had remained narrow throughout the year. On average, spreads averaged 32-35 basis points over the AAA Municipal Market Data (MMD) spot. In contrast, the more volatile nature of 2023 positioned this year as a relative haven for investors seeking stability.

Significantly, returns in the single-A category have eclipsed broader index performances, with Bloomberg Barclays’ A-rated index outpacing AAA-rated bonds by a notable margin. This churn in yield dynamics underscores the essential lesson for investors: credit quality does not always correlate directly with performance, particularly in an evolving market landscape that continuously adapts to external pressures.

As municipal bonds close out December, the future remains steeped in uncertainty. Market participants are urged to remain agile and discerning, mindful of the implications of prospective fiscal policies and interest rate movements. The interplay between limited supply, evolving demand dynamics, and the broader challenges associated with Treasury yields will determine the trajectory of the municipal bond space as we enter 2025. Understanding these complexities will be critical for investors aiming to navigate this competitive environment successfully.

Leave a Reply