As the week comes to a close, municipal bonds have exhibited stable characteristics despite the overall mixed signals prevailing in the broader financial markets. The last significant deals of the week have been priced favorably while municipal bond mutual funds have reported 13 consecutive weeks of inflows, primarily driven by high-yield categories. Interestingly, the performance of municipal bonds appears to stand distinct from the rather tumultuous behavior of U.S. Treasury securities, which have been experiencing fluctuations of their own.

Municipal bonds remain steadfast in their trajectory, signaling resilience. The latest ratios comparing municipal bonds to U.S. Treasuries reveal a steady landscape. For instance, specific maturity ratios such as the two-year and three-year maturities are resting at 64%, while the longer end, including the 30-year bonds, is at 85%. These percentages, derived from Refinitiv Municipal Market Data, indicate a well-defined niche for municipal bonds amidst a choppy Treasury market. ICE Data Services provided almost identical figures, reinforcing the notion that municipal bonds maintain their own steadiness in the current financial milieu.

A critical aspect of this stability stems from the absence of pressure that typically drives municipal rates upward. Kim Olsan, a senior fixed-income portfolio manager at NewSquare Capital, brought attention to a noteworthy decline in daily bids compared to the year’s average, decreasing by 15%. This is set against the backdrop of issuance expected to surpass $40 billion for September, a significant jump from the decade’s average of $34 billion. This month’s bond activity suggests that while issuance is robust, demand remains strategic and tempered.

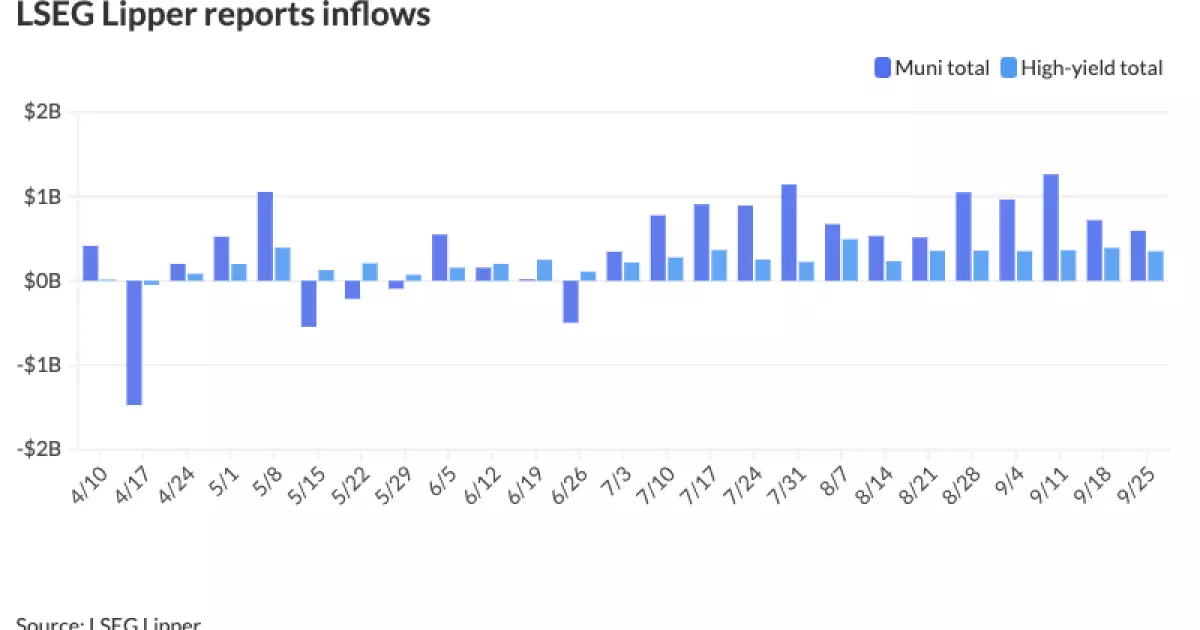

Additionally, mutual fund flow figures have displayed a strong inclination towards inflows, with approximately $8.8 billion entering the market this quarter alone. The Investment Company Institute reports largely positive trends, with only a single week breaking the pattern of inflows. For the week ending on Wednesday, LSEG Lipper indicated that investors have added $592.1 million to these funds, following a strong previous week of $718.4 million. This continued uplink in inflows is crucial in solidifying the municipal bond market’s health and attractiveness.

High-yield municipal bonds have emerged as a focal point of strength within the market, demonstrating significant inflows of $349.2 million after recording $389.7 million in the preceding week. This uptick is indicative of a recovery toward normalization after a staggered performance earlier in 2023, where issuance was noted at a stark $7.6 billion. The current figures nearly align with the trailing five-year average of approximately $20.1 billion which enables high-yield bonds to regain investor confidence and market presence.

Moreover, the demand for yield-focused instruments appears to exceed available supply, further underscoring the persistent interest in municipal high-yield offerings. According to strategists at J.P. Morgan, inflows into this segment have reached about $12 billion, representing a strategic allocation in a landscape where traditional corporate bonds struggle to provide comparable returns. The ongoing replaceability of cash into municipal offerings by sidelined investors suggests an eagerness to capitalize on potential yield curves.

As September concludes, historical patterns might shift, especially given the expectations around upcoming supply heading into the next month. Olsan posits that the significant issuance anticipated could have an impact on yields, but these movements may remain controlled in the short term. Tax-sensitive investors are particularly eyeing opportunities in the AA-rated bonds trading at around 2.75%, which translates to a taxable equivalent yield of approximately 4.50%.

Illustrating the above dynamics, offerings such as the Salt River Project Agricultural Improvement and Power District of Arizona reveal the competitive edges of longer-term bonds, with 5s of 2034 yielding at 2.72% and those of 2049 at 3.64%. This refreshes interest in larger issues providing attractive coupon structures beyond 15-year durations, evidently spurred on by solid backing from both individual and corporate investors.

In this unique period of stability within the municipal bond sector, the interplay of inflows, stable ratios, and the emerging high-yield strength indicates that the market is on solid ground. This landscape is especially promising for those seeking better yield opportunities compared to ventures in the corporate bond space. As the month wraps up and the market braces for potential changes, the ongoing interest in municipal bonds signals a readiness by investors to engage with this asset class actively. The evolutionary trends observed promise rewarding potential amid the broader financial currents.

Leave a Reply