As the municipal bond market navigates the final stretch of the year, it faces increased selling pressure while still managing to outperform U.S. Treasuries (USTs). This phenomenon is particularly noteworthy as it highlights the relative strength of municipal bonds in the current economic landscape. Despite an overall decrease in returns pushing the market into negative territory for the month, municipals remain more resilient compared to both USTs and corporate bonds. On Friday, yields for Triple-A rated municipal bonds saw modest increases ranging from three to eight basis points, correlating with a broader trend where losses in USTs were recorded between six to eight basis points.

Market ratios, which illustrate the relationship between municipal yields and UST yields, reflected these shifts. For instance, the two-year municipal to UST ratio stood at 61%, while the 30-year ratio noted an impressive 80%. Such ratios are crucial as they provide insights into the relative value of tax-exempt securities in the context of interest rate movements and investor sentiment.

Investor behavior throughout the week indicates a cautious stance, as reported banter around bid-wanteds hitting their highest levels in over a year suggests a strategic retreat from risk. Mikhail Foux from Barclays underscores this caution, noting that even amidst a heavy supply week, the market exhibits signs of fatigue, leading investors to reassess their exposure. The sentiment within the market has become pivotal as it impacts both current investments and future issuance.

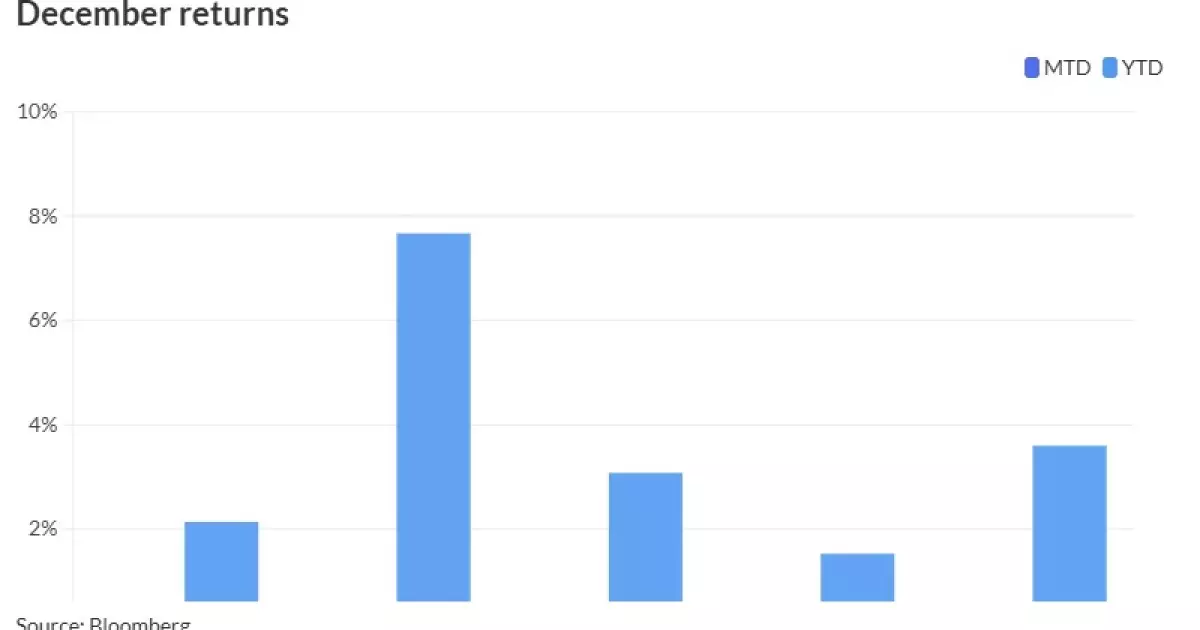

Despite the setbacks experienced this month, the Bloomberg Municipal Index displays a year-to-date uptick of +2.14%. However, the stark contrast between taxable munis and tax-exempt instruments has further complicated investor strategies, especially as taxable munis showcase a return of -1.01% for December. In light of these dynamics, market analyst reports from BofA Global Research suggest that a potential rally for the municipal market could gain traction following the upcoming Federal Reserve meeting, as the tide of new issuance begins to align with traditional holiday patterns.

Delving deeper into sector performance, the month-to-date analysis illustrates an even performance across the tax-exempt investment-grade (IG) bonds and municipal high-yield sectors. Still, a significant gap remains for the latter in terms of yearly returns, which showcases a striking underperformance of nearly 600 basis points thus far in 2024. Observations from BofA indicate that among IG ratings, BBB-rated returns have outperformed others for the month, reiterating the intricate dynamics of risk and return within the market.

Issuance trends also reveal a substantial growth trajectory this year, with a total of $493 billion recorded as of mid-December, representing a remarkable 32% increase year-over-year. This boost underscores the active participation of various investment classes, including mutual funds and foreign investors, although traditional bank ownership shows a decline. With the anticipated reduction in new issuance for the forthcoming week estimated at $2.5 billion, driven primarily by a high-grade transaction from New York City, market participants are poised for adjustments in strategy.

Looking ahead, the prevailing mood anticipates potential market shifts driven by monetary policy changes. Futures market projections indicate a probable rate cut in December, followed by several pauses and subsequent cuts in early 2025. This scenario suggests a favorable backdrop for continued bond market rallies, implying a further flattening of yield curves in the coming months.

However, market professionals like Foux caution about chasing performance amid uncertainties, advocating for prudent investment strategies as we approach late December. The continuation of a supply drought is expected to bolster prices in the short term, yet it remains crucial to evaluate broader economic indicators and the Fed’s moves that may influence overall performance.

The appetite for municipal bonds remains resilient, as evidenced by current trends. The potential for better opportunities may encourage investors to recalibrate their portfolios, particularly as significant issuances from various financing authorities loom on the horizon. As this complex yet engaging market continues to evolve, stakeholders should remain vigilant to capitalize on opportunities while managing inherent risks effectively.

Leave a Reply