As the calendar year unfolds, the dynamics surrounding municipal bonds have taken a notable turn, reflecting broader economic concerns and expectations about upcoming Federal Reserve actions. Recent market trends underscore a growing apprehension about interest rates and their implications for the financing landscape of local governments.

On Tuesday, the municipal bond market displayed signs of weakness, reacting to recent developments within the broader economy. Significant players, such as the New York City Transitional Finance Agency, took center stage as they priced their last significant issuance for 2024. Investors now find themselves in a precarious position, as mixed reactions in U.S. Treasuries and significant equity losses raise questions about the stability of the financial landscape. Anticipation mounts ahead of the Federal Open Market Committee’s (FOMC) impending rate decision, where many expect a reduction of 25 basis points. However, mixed feelings arise concerning the potential trajectory for future cuts as analysts weigh their expectations.

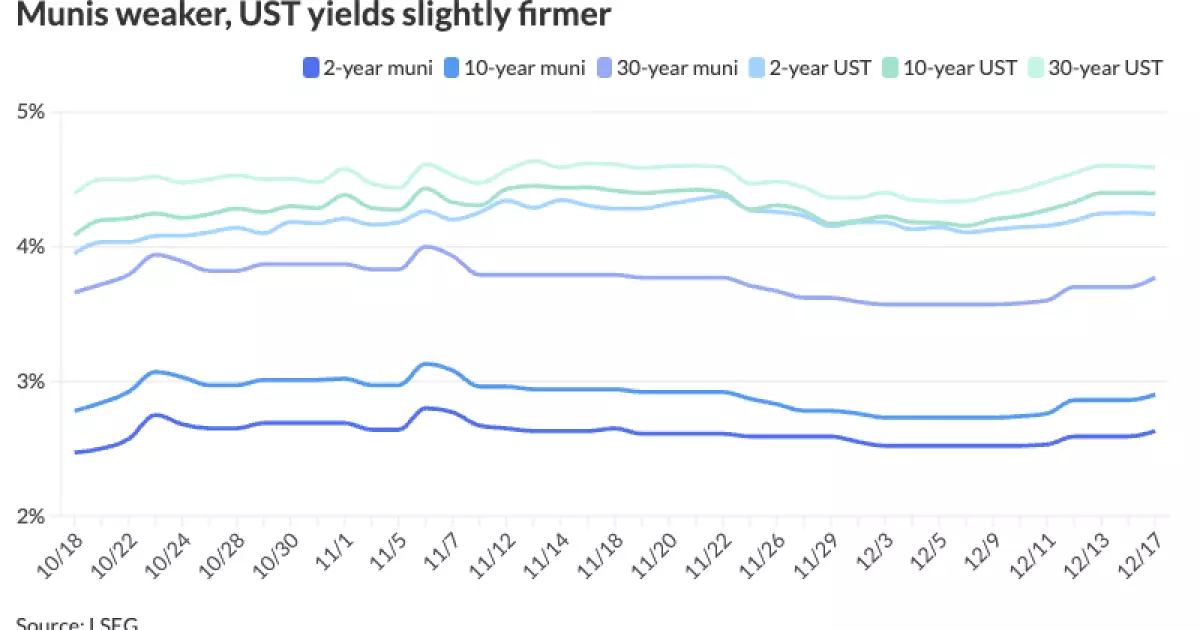

With increases of two to seven basis points in triple-A municipal yields, market indicators reflect a cautious atmosphere. Ratios comparing municipal bonds to U.S. Treasury rates have also experienced upward adjustments, signaling a shift in investor sentiment. For instance, the two-year municipal-to-Treasury ratio now stands at 62%, while the 30-year figure is at 82%. These shifts illustrate a growing concern among investors, who are grappling with the implications of potential rate cuts, especially in light of economic data that may influence future monetary policy decisions.

Conversations around U.S. Treasury (UST) supply and demand continue to loom large over market dynamics. According to the Congressional Budget Office, the next decade will necessitate an additional $22 trillion in UST supply to cover projected deficits. This situation raises alarm bells as expectations of an additional $4 trillion to $14 trillion in federal deficits materialize, exacerbated by tax cuts and ongoing financial obligations. Analysts like Matt Fabian from Municipal Market Analytics assert that this projected increase in UST issuance could, at least, double the current outstanding total by 2034.

As these figures emerge, it becomes clearer why recent sell-offs in the UST market have not only seemed rational but perhaps necessary. With mounting pressures on tax-exempt municipal bonds stemming from a late-year new-issue calendar, investors are beginning to voice their concerns about the viability of tax exemptions in the coming year. As the market shifts toward the anticipation of heightened issuance in early 2025, it is crucial for municipal issuers to navigate these financial currents with precision.

Future Implications for Municipal Financing

Despite the turbulence, forecasts remain somewhat optimistic regarding municipal finances. While the supply of municipal bonds is expected to grow, primarily to fund essential infrastructure projects—ranging from airports to bridges—municipalities appear to be in solid financial standing. This positions them uniquely as they seek to manage the impending influx of bond issuances without sacrificing their fiscal health.

Recent data suggest that total municipal bond issuance may soon reach the $500 billion mark for the year. This potential rise underscores a significant uptick in infrastructure development projects, which might positively influence local economies. Key upcoming deals slated for January include substantial offerings from the San Francisco International Airport and the University of California, which could invigorate the market as municipalities harness opportunities for long-term growth.

Investor sentiments have shifted as many speculate on the Federal Reserve’s forthcoming decisions. There is a growing belief that the anticipated rate cut could be the last for an extended period, which influences market dynamics significantly. As analysts like Giles Nicholson suggest, the immediate focus has pivoted not only to the likelihood of a cut but also to the subsequent implications it might carry for economic health. If future cuts appear doubtful, market participants might interpret this as an optimistic signal regarding the economy’s performance.

As stakeholders await potential clarifications from Federal Chair Jerome Powell’s speeches, the situation remains fluid. Shifts in the anticipated economic landscape could either bolster or dampen investor enthusiasm, reinforcing the need for a vigilant approach amidst uncertainty. Overall, the current municipal bond environment is characterized by a cautious outlook, with a significant emphasis placed on Government policy directives and economic data that may shape future financial opportunities.

As we move forward, market participants must remain agile and well-informed, keeping a close watch on developments as this year unfolds, particularly concerning the complexities entwined in interest rate adjustments and their cascading effects on municipal financing.

Leave a Reply