As we dive deeper into the year 2024, the financial environment surrounding Build America Bonds (BABs) is characterized by considerable volatility and challenges. Factors such as rising interest rates, increased market ratios, and economic fluctuations are influencing both issuance and redemption of these bonds. Despite these hurdles, a number of issuers remain determined to call back their BABs before the year concludes, indicating a complex but dynamic landscape in municipal finance.

The current environment for BABs is marked by a significant slowdown in redemptions, reflecting a broader trend in the municipal bond market. With approximately $14.9 billion of BABs called in 2024 thus far and another $938.3 million in the pipeline, it’s clear that despite the redemptive challenges, actions are still being taken to manage these investments. According to insights from J.P. Morgan, about 39 issuers have engaged in deals to refund their outstanding BABs this year, signaling ongoing interest but also caution among issuers due to the economic landscape.

Earlier in the year, projections suggested that nearly $30 billion of outstanding BABs were viable candidates for extraordinary redemption, boosted by a favorable court ruling that eased certain restrictions. However, the deciding factor for issuers remains economic viability. As noted by Nick Venditti, head of Municipal Fixed Income at Allspring, the economic rationale for refunding bonds is compelling only when prevailing rates are significantly lower than those currently observed. For instance, with the 10-year U.S. Treasury yielding 4.27% amid a recent selloff in the municipal market, the likelihood of yielding substantial cost savings through refundings appears diminished.

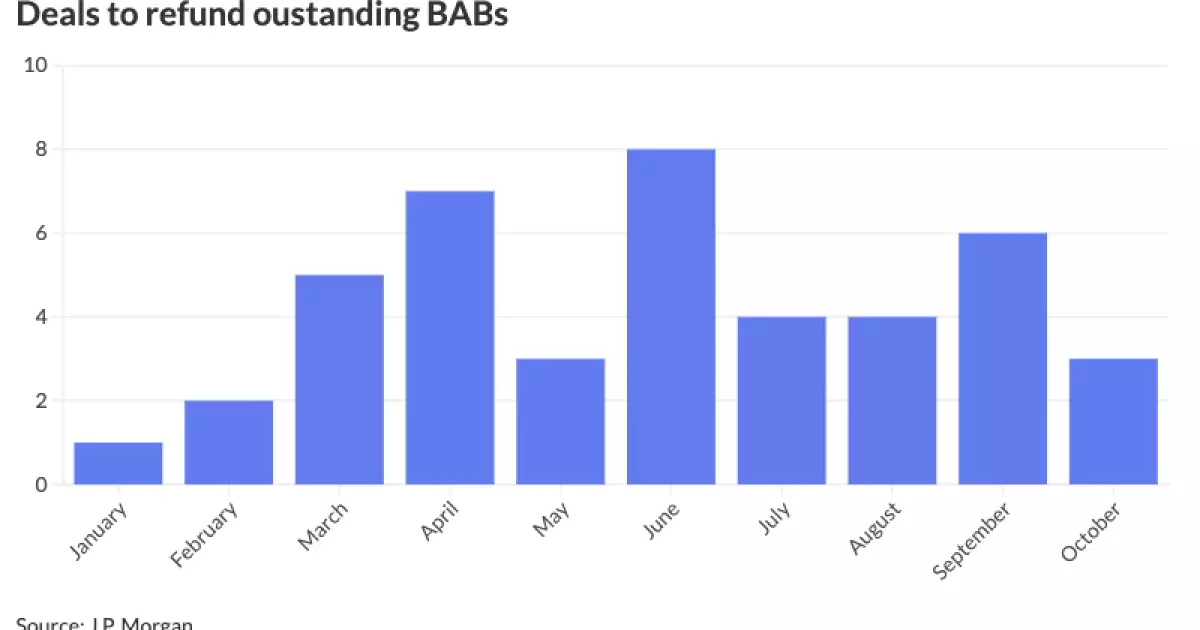

Analyzing the trends in BAB refundings, it’s apparent that 2024 began sluggishly, particularly in the first quarter. However, a noteworthy spike occurred during the second quarter, which was followed by a retracement in the third quarter. Data shows that June was particularly active, with eight refunding transactions, while other months like April and October saw a comparatively lower number of active deals.

The Los Angeles Unified School District topped the charts with a significant refunding activity, issuing $2.9 billion in general obligation refunding bonds in late April. This monumental deal reflects both the need and capacity of certain issuers to capitalize on market conditions, even as rising interest rates dampen enthusiasm for such actions broadly. Notably, market experts, including James Pruskowski of 16Rock Asset Management, have observed a marked decline in the popularity of BAB refinancings after the second quarter, attributing this shift to rising interest rates and a seasonal slowdown in the third quarter.

One key influencing factor in the BAB market has been the prevailing market volatility. A notable instance was seen with the Ohio Water Development Authority, which postponed a $102.02 million transaction due to unforeseen market conditions, which were estimated to potentially lead to minimal or even zero net present value savings. Mike Fraizer, executive director of the Authority, articulated that the intention was to wait until market conditions stabilize to ensure that their financial objectives are met effectively.

Interestingly, even amidst notorious legal challenges, such as the lawsuit threats faced by the Regents of the University of California, many issuers have proceeded with their plans to refund BABs. For example, the University continued with their call scheduled for March 27, showcasing the determination among issuers to navigate their financing strategies adeptly despite external pressures.

The current atmosphere surrounding BABs appears increasingly fraught with uncertainty. Market analysts, such as Venditti, have underscored the diminishing attractiveness of BABs from the perspective of institutional investors, particularly in light of the inherent call risks. These risks create a perception that BABs are becoming “almost uninvestable” unless there are legislative assurances that solidify their call provisions.

Looking ahead, the attractiveness of taxable munis is rising among institutional investors, who are exploring alternatives in a bid to align assets with liabilities. As BAB refunding activity dwindles due to market conditions, issuers and investors alike must evaluate their strategies and anticipate further changes in the market dynamics, as each move could potentially reshape their financial landscapes in the months to come.

While the Build America Bond market grapples with significant challenges, it remains an area of active interest and strategic maneuvering for many issuers. The steps taken today will undoubtedly influence the future trajectory of BABs within the broader municipal finance ecosystem.

Leave a Reply