While most investors have been mesmerized by the seemingly stable yields on Treasuries and the impressive rally in corporate bonds, the municipal bond sector tells a far more troubling story. Despite the apparent resilience of other fixed-income classes, munis are quietly suffering a notable depreciation—down nearly 4% for the long-dated indices, far worse than their peers. This divergence isn’t just noise; it is a systemic indicator that something fundamental is amiss beneath the surface of what many consider a steady, tax-advantaged asset class. Such underperformance, especially amid rising rates and abundant issuance, should serve as a clarion call for skeptics and proponents alike to reevaluate the true health and stability of municipal bonds.

Unlike corporate bonds or Treasuries, which benefited from falling yields and supply constraints, munis faced a perfect storm of oversupply early in the year. Issuers, spooked by potential tax law changes and prior pandemic aid reductions, flooded the market with $280 billion worth of new debt. This frontloading artificially inflated issuance, widening spreads and distorting the yield curves. Yet, with the contentious tax tactics now settled and the exemption intact, the market’s recent underperformance hints at deeper structural issues rather than mere short-term jitters. Could the muni sector be suffering from an inherent liquidity crisis, or is it simply a reflection of investors’ changing risk appetite?

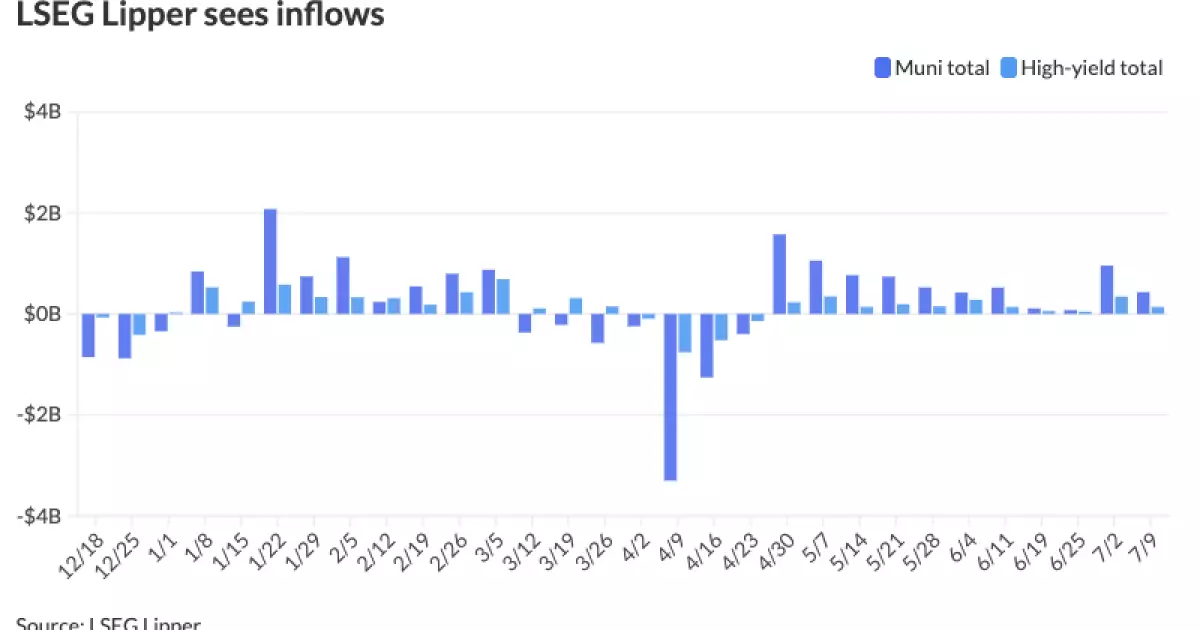

The market’s peculiar behavior—long munis underperforming substantially with steepening curves—points toward more than just bad timing. Instead, it suggests a hesitancy among institutional investors to extend beyond the 15-year maturity horizon. The recent rally in fund flows into municipal bond funds and tax-exempt money market funds isn’t enough to stem the tide of waning confidence, particularly in the longer end. This suggests a potential structural shift: investors yearning for safety, but wary of the risks wrapped up in long-term municipal debt, especially amid inflationary pressures and ongoing fiscal uncertainties at the local government level.

Supply Dynamics and Political Realities: The Roots of Muni Market Turbulence

The surge of issuance in the first half of the year might have temporarily masked the underlying vulnerabilities, but the true story is more nuanced. Municipal bonds are inherently tied to local politics, fiscal policy decisions, and socio-economic conditions that differ sharply from federal bonds. When local governments issue debt en masse, often driven by immediate needs like infrastructure, schools, or healthcare, they risk creating a glut that dampens valuations and liquidity over time. The recent slowdown in new supply likely won’t mend the bleeding in the long-term muni indices, which are struggling to recover from the steep sell-off.

Moreover, the political climate continues to shape—sometimes distort—the muni market. With a backdrop of fiscal austerity, debates on state and local tax policies, and the lingering influence of pandemic relief conditions, municipal issuers are caught in a constraining web of uncertainty. The traditional view of munis as ‘risk-free’ or at least ‘low-risk’ is being challenged by reality: local governments are pressured by falling revenues, reduced aid, and inflationary fundraising costs. These headwinds mean that even with the tax exemption secured, the bonds themselves don’t hold the safety aura they once did.

The steepening curves, especially in the long-end, reveal investor wariness. Market participants prefer shorter maturities to avoid exposure, indicating that the perception of long-term municipal risk has heightened. This shift isn’t purely tactical or temporary; it signals a potential reassessment of the entire municipal debt landscape, where the built-in assumption of safety is giving way to caution—or outright skepticism.

Implications for the Future: Is This the Beginning of a More Sustained Decline?

The persistent underperformance raises grave questions about the future trajectory of municipal bonds. Is this just a temporary correction in a sector that will eventually rebound as supply tightens? Or is this a harbinger of more profound structural change—a shift toward a less liquid, more risk-aware muni market? Many seasoned analysts believe the latter, especially if the current trends in yield curve steepening and withdrawal of long-term interest persist.

Fund flow data underscores this caution. Despite inflows into municipal mutual funds and tax-exempt money-market vehicles, these are primarily concentrated in short-term holdings—a clear sign of risk aversion. Investors are demanding higher premiums for longer maturities just to hold onto these assets, elevating spreads and making long munis less attractive. If this trend continues, the market could face a widening gap between the perceived and actual value of municipal debt, leading to a vicious cycle where even moderate supply or economic shocks trigger outsized price declines.

The potential policy implications are significant. Should rates begin to fall in the coming months—perhaps as the Federal Reserve signals an easing stance—the muni market might see a temporary rally. But without addressing the core issues—overissuance, fiscal fragility at local levels, and investor complacency—the sector risks being permanently impaired. A market that once thrived on stability and tax advantages could turn increasingly volatile and fragmented as investors recalibrate their expectations and risk models.

In essence, the municipal bond market is at a crossroads. The recent underperformance and structural shifts in investor behavior hint that the sector’s old assumptions are no longer valid. A cautious, center-right stance urges policymakers and investors not to dismiss the signs—because the current turmoil is more than just market volatility; it is a fundamental reevaluation of municipal debt’s role in a diversified portfolio and a resilient public finance landscape.

Leave a Reply